Total income rose 44% to Rs 53.5 crore during the year, up from Rs 37.1 crore in FY25, according to an ICRA report.

The company's LAS book expanded to Rs 580 crore as of March 31, 2026, supported by Zerodha's large retail investor base and broking franchise.

ICRA reaffirmed Zerodha Capital's long-term rating at AA- (Stable) and short-term rating at A1+, while increasing the rated amount of its unallocated bank facilities to Rs 900 crore from Rs 600 crore.

"The stable outlook on the long-term rating reflects ICRA’s expectation that ZCPL will continue to benefit from the synergies arising from the Group’s established franchise and track record in capital markets," said the rating agency in the report.

Launched in 2021, Zerodha Capital offers loans against shares and mutual funds with ticket sizes ranging from Rs 25,000 to Rs 10 crore. The company lends against approved securities at loan-to-value ratios of up to 50%.

]]>The company allotted 2.61 crore equity shares to anchor investors at Rs 152 apiece, the upper end of its IPO price band.

The anchor round also saw participation from Amansa Holdings, Border to Coast Emerging Markets Equity Fund, Societe Generale, BNP Paribas Financial Markets, Susquehanna Pacific, Bajaj Finserv and Citi Group, among others.

Domestic mutual funds accounted for 42.5% of the anchor allocation, picking up 1.11 crore shares through 12 schemes across seven fund houses, while life insurance companies were allotted 35.72 lakh shares, or 13.67% of the anchor portion.

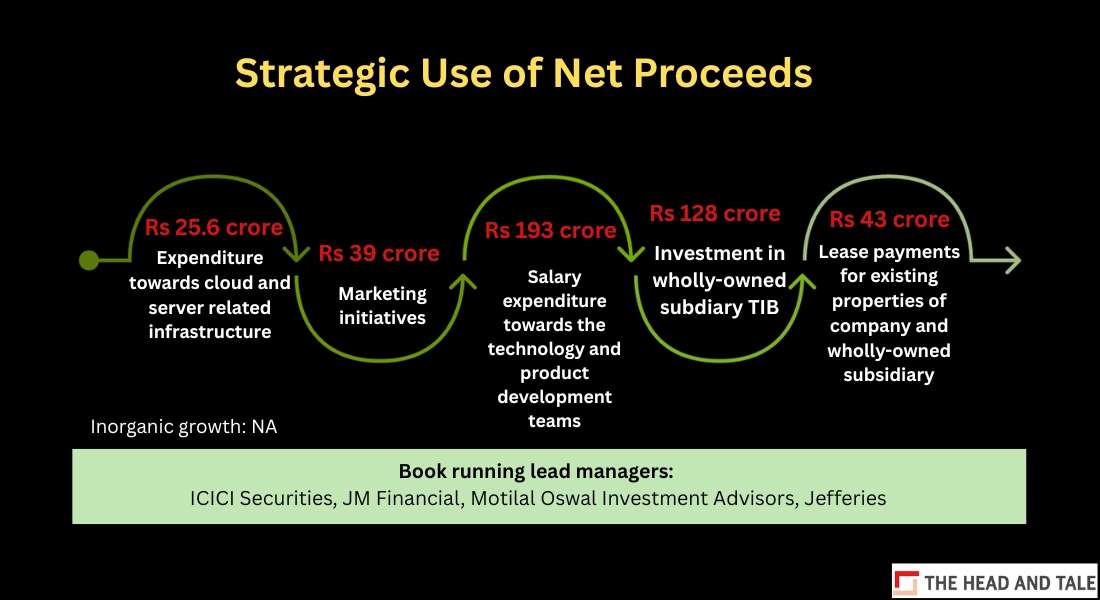

The Mumbai-based startup's IPO opened for subscription on June 19 and will close on June 23. As per its RHP, the public issue comprises a fresh issue of shares worth Rs 661 crore and an offer for sale (OFS) of 1.46 crore shares by founders and existing investors, taking the total issue size to Rs 883 crore at the upper end of the price band. The company had cut the size of its OFS.

The fresh capital will largely go towards funding its subsidiary Turtlemint Insurance Broking Services, working capital, lease rent for office spaces, and marketing and brand-building activities, besides general corporate purposes.

Turtlemint was founded in 2015 by Dhirendra Mahyavanshi and Anand Prabhudesai, who previously worked at ICICI Lombard/Quikr and Yahoo/Nokia, respectively. The startup runs a "phygital" insurance distribution model, pairing an online platform with a network of over 100,000 POSP advisors across tier-2 and tier-3 towns. It offers health, motor, life and travel insurance along with mutual funds, competing with the likes of Policybazaar, Acko and Plum.

]]>Both revenue and cash burn of the ChatGPT maker nearly tripled compared with the same period last year, underscoring the massive costs associated with developing and operating advanced artificial intelligence models.

The report said OpenAI's cash and marketable securities increased to more than $73 billion at the end of the quarter from about $40 billion at the end of 2025, boosted by a funding round announced in March.

The figures highlight the scale of investment required to compete in the AI race, as companies continue to spend heavily on computing infrastructure, model development and talent.

OpenAI's growing cash reserves come despite reports that the company recorded a net loss of about $39 billion in 2025.

Earlier this month, the Sam Altman-led AI company confidentially filed paperwork for an initial public offering (IPO), shortly after rival Anthropic also initiated plans to go public.

]]>As part of the collaboration, HSBC plans to develop more than 200 AI use cases over the next two years across areas such as wealth management, financial crime detection and employee productivity.

The bank will gain access to Google's Gemini AI models, while teams from Google Cloud and Google DeepMind will work with HSBC to identify and build projects with significant business impact. According to HSBC, individual initiatives could generate more than $100 million in additional revenue or cost savings.

HSBC said it plans to use AI to offer more personalised services to wealth management clients, strengthen anti-financial crime controls and reduce administrative work for frontline employees through tools that assist with tasks such as meeting preparation and research.

The bank currently runs around 600 applications on Google Cloud. The partnership builds on HSBC's broader efforts to integrate AI into its operations as banks increasingly adopt the technology to improve efficiency and customer service.

]]>The company's profit fell from Rs 408.1 crore in FY25, while its net worth increased 55% to Rs 916.1 crore, according to an ICRA ratings report.

ICRA said Raise Securities continued to post healthy profitability despite regulatory curbs on index derivatives trading and softer market conditions. However, higher operating expenses, including increased spending on marketing, team expansion and certain one-off costs, weighed on profitability during the year.

Founded in 2021 by former Paytm Money chief executive Pravin Jadhav along with Jay Prakash Gupta and Alok Pandey, Raise Securities operates stockbroking platform Dhan and options trading app Option Trader.

As of March 2026, the company was India's ninth-largest broker by active clients with a market share of 2.3%, according to ICRA.

The ratings agency assigned Raise Securities an A+ long-term rating with a stable outlook and reaffirmed its A1+ commercial paper rating.

]]>The initiative will function as a private-sector partnership, with the Financial Intelligence Unit-India (FIU-IND) participating as an observer.

The platform's secretariat will be jointly managed by the Payments Council of India (PCI) and the Fintech Convergence Council (FCC).

ARIFAC plans to focus on professional training, certification programmes, workshops, and awareness-building initiatives aimed at improving AML/CFT compliance standards across the financial sector.

The platform will bring together reporting entities from a wide range of sectors, including banks, non-banking financial companies (NBFCs), payment service providers, insurance firms, securities market intermediaries, cooperative institutions, and virtual digital asset service providers. The alliance seeks to encourage knowledge sharing, strengthen compliance capabilities, and support efforts to curb financial crimes while enhancing the integrity of India's financial system.

In addition, ARIFAC will establish dedicated working groups to address priority issues such as enhanced due diligence, sanctions screening, cross-border information sharing, digital banking risks, mule account detection, and virtual digital asset oversight. These groups will develop practical recommendations and industry frameworks for broader adoption.

The launch comes amid growing concerns over increasingly sophisticated financial crimes such as cyber-enabled fraud, money laundering, terrorist financing, sanctions violations, mule account networks, and risks associated with digital assets.

]]>The proposed IPO will be entirely an offer for sale (OFS), with existing shareholders looking to offload 14.89 crore equity shares. Since no fresh shares are being issued, NSE will not receive any proceeds from the public issue.

Shareholders participating in the sale include State Bank of India, Canada Pension Plan Investment Board (CPPIB), MS Strategic (Mauritius) Limited, Aranda Investments (Mauritius) Pte Ltd and Bank of Baroda, among others.

As of the draft filing date, Life Insurance Corporation of India (LIC) was NSE's largest shareholder with a 10.72% stake. Other key investors include Aranda Investments (Mauritius) Pte Ltd, Stock Holding Corporation of India Ltd and SBI Capital Markets Ltd.

The exchange has appointed 20 merchant bankers for the issue, including Kotak Mahindra Capital, Morgan Stanley, HSBC, J.P. Morgan, SBI Capital Markets, HDFC Bank and JM Financial.

For FY26, NSE reported revenue of Rs 16,601 crore, down 3% year-on-year, while profit after tax fell 15% to Rs 10,302 crore.

Once listed, NSE will join BSE as one of India's publicly traded stock exchanges.

The round also saw participation from existing and new investors including Accel, BoldCap, Nexus Venture Partners, Premji Invest, and Unbound. The company's early backers include Pushmeet Kohli, VP at Google DeepMind, and Sriram Rajamani, Corporate VP at Microsoft CoreAI.

The San Francisco-based startup will use the fresh capital to train its formalisation and prover models, expand its AI research team, and onboard domain experts across regulated sectors such as taxation, healthcare diagnostics, cybersecurity, and financial compliance.

Pramaana Labs was founded by IIT Madras alumni Ranjan Rajagopalan, Krishnan Raghavan, and Sanjay Ganapathy Subramaniam, who previously worked at Google Maps Moderation, Glean, and Google DeepMind (Gemini), respectively.

The company builds AI systems that convert complex domain knowledge, such as tax codes and clinical protocols, into machine-verifiable logic using the LEAN proof language, layered atop an LLM for natural-language flexibility.

"AI has an accountability gap," said Rajagopalan, co-founder and CEO of Pramaana Labs. He added that the rules governing domains like tax codes function much like mathematical rules, so once codified, the reasoning built on top of them becomes deterministic rather than probabilistic.

Khosla Ventures Founder Vinod Khosla said auto-formalisation addresses a capability AI currently lacks.

]]>The two companies, it notes, differ in size, scale, operating history, business model, capital resources, customer acquisition channels and stage of growth.

That argument is reasonable, particularly given the nature of the market. Insurance penetration in India remains low, with significant headroom for growth across both life and non-life segments. Distribution, in particular, continues to be fragmented and underdeveloped, leaving room for multiple models and players to scale.

Yet, even within this broader opportunity, Turtlemint’s own operating performance presents a more mixed picture.

For one, the company continues to incur losses, which it identifies as a key internal risk, alongside negative operating cash flows and a declining net worth.

While Indian initial public offering (IPO) markets have traditionally favoured profitable companies, regulations under the Securities and Exchange Board of India (SEBI) have for several years allowed loss-making firms to list, subject to higher institutional participation. This route has increasingly been used by new-age technology companies in recent years.

Notably, PB Fintech was also loss-making at the time of its IPO filing in 2021.

Besides, Turlemint’s substantial over 8x jump in its revenue from operations in FY25 has come on the back of a quietly engineered internal acquisition. In May 2024, Turtlemint’s parent firm Turtlemint Fintech Solutions Ltd (formerly Fintech Blue Solutions Pvt Ltd) acquired its subsidiary Turtlemint Insurance Broking Services Pvt Ltd (formerly Invictus Insurance Broking Services Pvt Ltd) from its promoter, Dhirendra Mahyavanshi. (We have broken down the independent financials of the two entities later in the article.)

The acquisition has also triggered shifts in its revenue mix and structure that make its financials less directly comparable periods. Investors typically look for three to five years of stable, comparable financial data. Here, however, the “full” business effectively exists only post-acquisition, even if the transaction itself was internal.

Turtlemint’s model also carries structural cost pressures. Turtlemint’s heavy reliance on its network of digital partners, while central to its distribution strategy, translates into significant acquisition and retention costs.

Beyond this, a range of risks continue to weigh on the business. These include its heavy dependence on motor insurance and top insurers, concentration in a few key states, GST-related exposure and regulatory constraints as it approaches the public markets.

While the company has expanded into adjacent segments such as mutual funds and lending, these remain early-stage and operate in already competitive markets.

Artificial intelligence (AI), which the company is actively investing in, also presents a double-edged sword. The same technologies that can improve productivity may lower barriers to entry, enabling new players to replicate similar models and intensify competition, not just from established platforms like PB Fintech but also from emerging startups.

Before examining these risks in greater detail, it is worth looking at the strengths that have brought the company to the cusp of the public markets.

Origins and funding

Founded in 2015 by Dhirendra Mahyavanshi and Anand Prabhudesai, both of whom previously held senior management roles at Quikr, Turtlemint set out to organise India’s fragmented insurance distribution ecosystem through a digital-first approach.

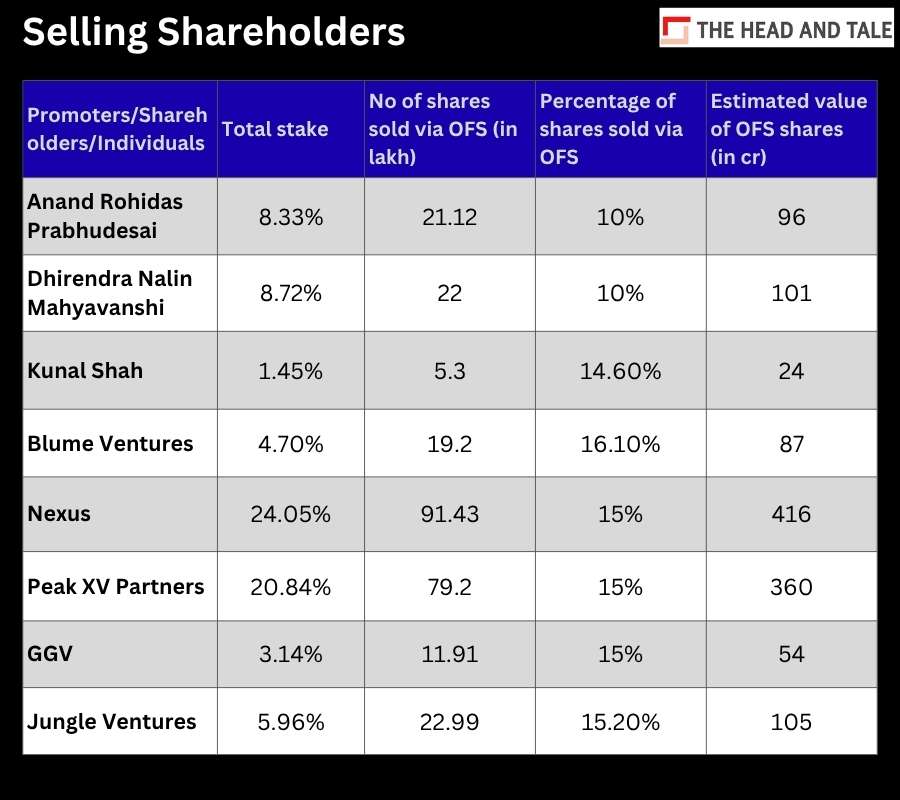

The company raised its first institutional funding in early 2016, led by Nexus Venture Partners with participation from Blume Ventures, and went on to attract marquee investors including Peak XV Partners, Jungle Ventures and GGV Capital. This culminated in a $120 million Series E funding round in 2022, valuing the company just shy of the $1 billion mark.

The IPO now provides partial liquidity to these early backers. Nexus Venture Partners and Peak XV Partners alone are estimated to realise around Rs 416 crore and Rs 360 crore, respectively, through the offer for sale (OFS). The amount Nexus and Peak XV are taking out exceeds their cumulative investments of Rs 247 crore and Rs 111.5 crore, respectively, according to Tracxn.

The offering also comes amid a broader wave of new-age listings, where public markets have increasingly doubled up as liquidity events for early investors. In Turtlemint’s case, this is evident in the OFS, even as the company raises fresh capital to fund its next phase of growth.

Business model

Unlike Policybazaar which operates a B2C digital marketplace model that directly enables consumers to compare and buy insurance, Turtlemint operates a hybrid model that keeps agents or what it calls ‘Digital Partners’ at the centre of its business model.

Turtlemint had 603,302 Digital Partners, including 484,832 the point-of-sale persons (PoSPs), as of September 30, 2025. These Digital Partners have completed mandatory training enabling them to obtain the requisite certification to distribute insurance products in accordance with applicable regulatory guidelines.

Notably, as of September 30, 2025, 80.05% of its Digital Partners were based in B30+ markets and 74.79% of platform premium distributed sold in B30+ markets. Its B30+ markets refers to the rest of India except top 30 cities by population.

While the presence of well-trained Digital Partners is crucial in a country like India where financial literary in low especially in non-metro markets, the cost of maintaining them is also pretty steep.

The cost of acquiring and retaining Digital Partners increased to 76.58% of its total expenses in the six months period ended September 30, 2025 from and 62.51% in September 30, 2024.

The company draws comfort from its relatively strong retention rates of these Digital Partners. It said that 69.46% of its Digital Partners remained active i.e. it continued to receive payouts from the company after two fiscals following their onboarding in FY20. Further, 64.04% remained active after five fiscals ended FY25 following their onboarding. “We believe that these high retention rates enable us to achieve strong returns on our investments in recruiting, training and supporting our Digital Partners,” said the UDRHP.

Even so, the cost burden associated with this model remains a key constraint, with the pressure on profitability unlikely to ease meaningfully in the near term.

Independents financials before the internal acquisition

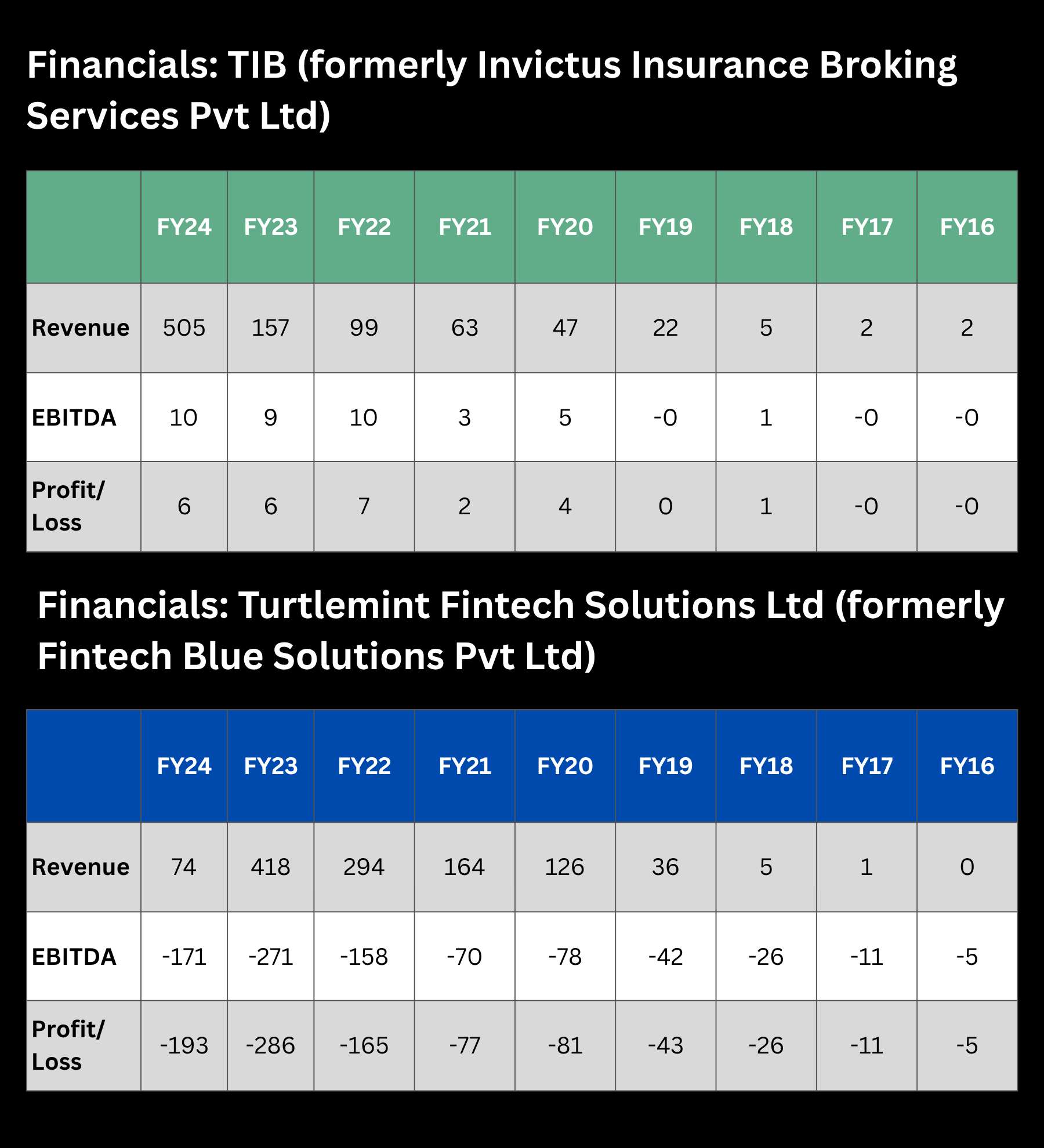

Before we dive into the financials of the company disclosed in the UDRHP, let us separately look at the financials of Turtlemint Fintech Solutions Ltd (formerly Fintech Blue Solutions Pvt Ltd) and its acquired subsidiary Turtlemint Insurance Broking Services Pvt Ltd (formerly Invictus Insurance Broking Services Pvt Ltd). [We are using ‘TIB’ for future reference in the story].

In the year before the acquisition happened, Turtlemint Fintech Solutions’ revenue from operations had plunged drastically to Rs 74.05 crore in FY24 from Rs 417.76 crore in FY23. The company’s operating revenue had been rising steadily till FY23 (see chart). However, the company’s net loss remained high as Rs 192.6 crore in FY24 and Rs 285.55 crore in FY23.

In contrast, Turtlemint Insurance Broking Services has been in the black since FY18 even as the net profit was just at Rs 6.22 crore in FY24. Notably, it was in FY24, that the subsidiary had seen its biggest jump in revenue to Rs 505.05 crore from just Rs 156.56 crore in FY23.

The timing of the acquisition is therefore notable, coming at a point when the parent’s operating performance had weakened even as the subsidiary’s business scaled rapidly.

TIB acquisition

The UDRHP says that Turtlemint acquired TIB with effect from May 8, 2024 from one of its promoters, Dhirendra Nalin Mahyavanshi, and accordingly, it does not have a long consolidated operating history through which its overall performance may be evaluated.

Turtlemint relies on TIB for its insurance broking business. TIB contributed 97.36% and 111.36%, of our revenue from operations in the six months period ended September 30, 2025 and September 30, 2024, respectively, and 96.32%, 89.52% and 29.10% of its proforma revenue from operations in fiscals 2025, 2024 and 2023, respectively.

“If TIB’s operations do not generate the expected returns or face adverse developments, our business, financial condition, results of operations and cash flows could be negatively impacted,” it noted.

The acquisition of TIB marked a pivotal shift in the company’s structure, but it also introduced a layer of complexity for investors assessing its performance. While the transaction effectively consolidated the core operating business under one entity, it shortened the track record of the combined company, making historical comparisons less reliable.

The company also discloses pro forma financials to illustrate how the combined entity might have performed historically. However, these are based on assumptions and are explicitly stated to be indicative rather than definitive.

Taken together, investors are effectively evaluating a combined entity with limited real operating history, relying partly on reconstructed and hypothetical financials.

UDRHP financials of combined entity

It is worth noting that Turtlemint has presented both restated and pro forma financials in its disclosure. Pro forma numbers reflect adjusted financials based on certain assumptions, typically to account for structural changes such as acquisitions, and may not be directly comparable with historical reported figures.

While it is not uncommon for companies to present both sets of numbers -- fintech company Pine Labs, for instance, had also disclosed similar adjustments when it filed its DRHP last year -- we have relied primarily on restated financials for the purpose of this analysis, unless stated otherwise.

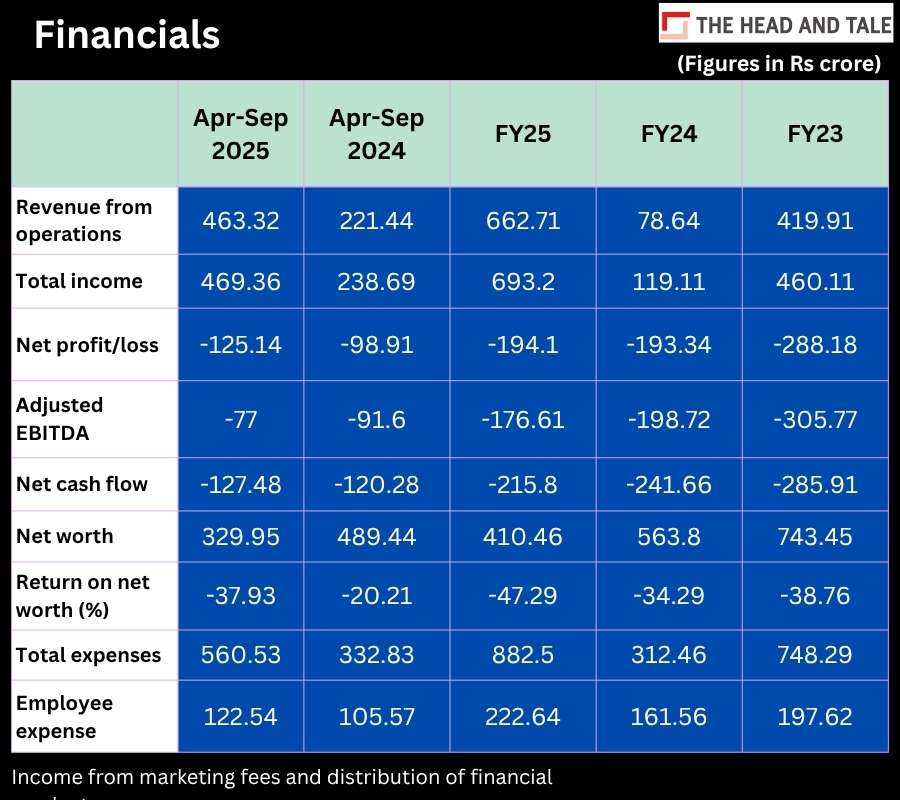

Turtlemint’s revenue from operations grew significantly over eight times year-on-year to Rs 662.71 crore in FY25. In the six months ended September 30, 2025 as well, its revenue from operations jumped to Rs 463.32 crore from Rs 221.44 crore in the same period in 2024. However, the company’s net loss has expanded.

Besides, the company has had negative cash flow in the past three fiscals through FY25 as well as in the six months ended September 30, 2025 and its net worth decreased from as of March 31, 2023 to September 30, 2025 due to the losses.

“If we are unable to generate adequate revenue growth and manage our expenses and cash flows, we may continue to incur losses and our business, financial condition, results of operations and cash flows may be adversely affected,” the company said in its UDRHP.

Change in revenue mix due to regulatory shifts

This challenge is further compounded by a shift in the company’s revenue mix.

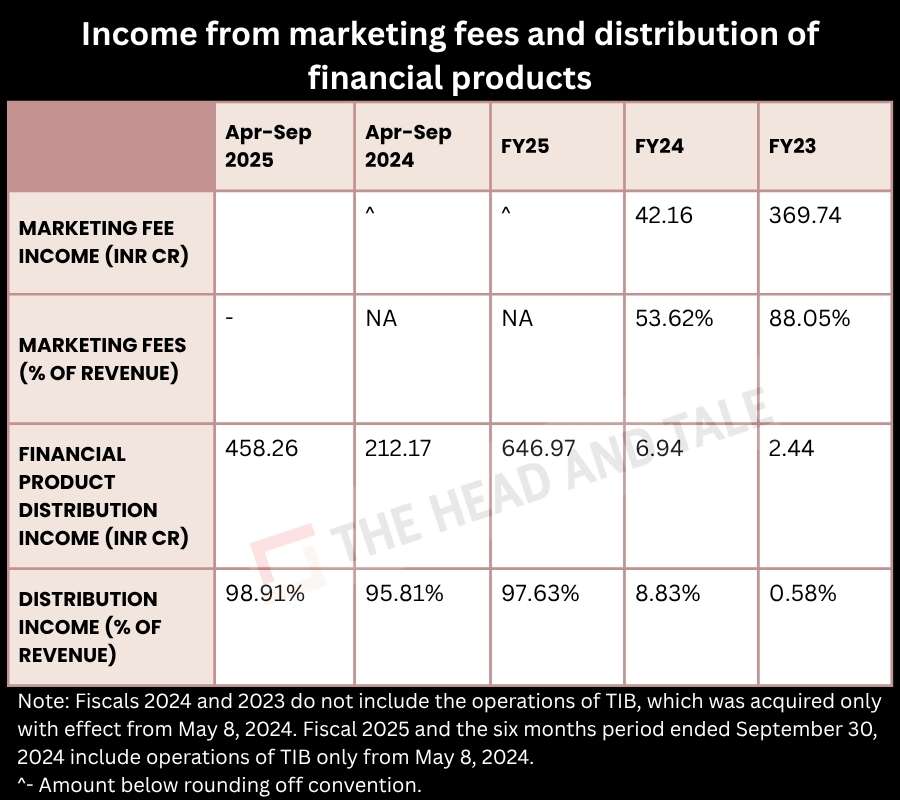

Until FY23 and even into FY24, the business was largely built around marketing fees (income from marketing fees refers to the revenue generated from online marketing, advertising and other related services provided to its Insurer Partners), which at one point contributed as much as 88% of revenue. That model was disrupted following regulatory changes that altered how insurers engage with distribution platforms. In April 2023, the Insurance Regulatory and Development Authority of India moved away from fixed commission structures to an overall expense cap (EOM), forcing insurers to tightly manage total spending. As a result, discretionary spends such as marketing fees declined, directly impacting platforms dependent on this revenue stream.

Post-acquisition of TIB in May 2024, income from distribution of financial products, largely commissions from insurance sales, came to account for nearly the entire revenue base, rising to upwards of 95-98%.

More importantly, the new model introduces a different risk profile. Commission-based income is inherently dependent on insurer behaviour, regulatory frameworks and payout structures, all of which lie outside the company’s direct control.

The company in the UDRHP noted that in the ordinary course of its business, it is subjected to periodic adjustments and revisions to the commissions and fees paid to it by its insurer partners.

“These changes may be made unilaterally by our Insurer Partners and can materially impact our revenues,” it stated.

For example, a general insurer reduced their commission rates on select motor insurance product from 32.50% as on August 1, 2023 to 30.00% as on August 1, 2024. Such instances resulted in a reduction in commission payouts to our PoSPs. These adjustments are typically made in response to changes in regulatory requirements, economic and competitive factors, or the Insurer Partners’ own business strategies.

Competition, attrition and AI risks

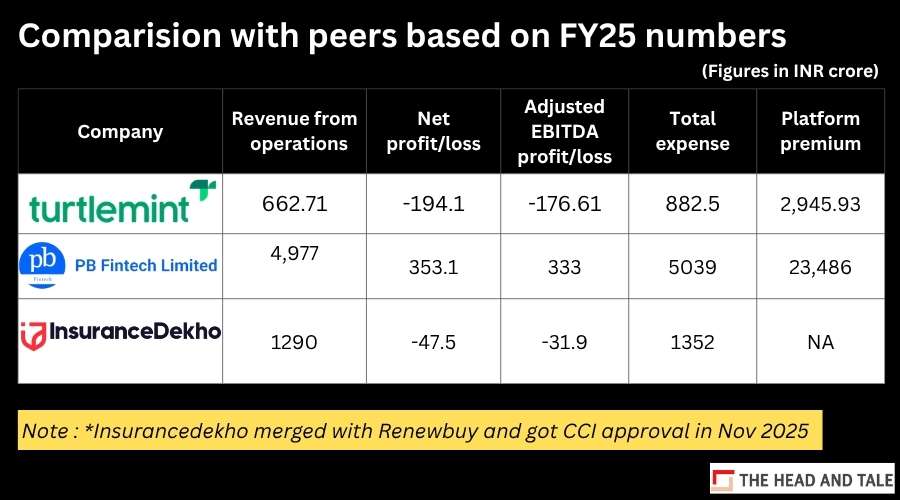

Competition in the insurance distribution space remains intense and fragmented. While PB Fintech is the only listed peer, the competitive landscape extends well beyond a single comparable, spanning insurers’ in-house channels, traditional agents, web aggregators and a growing set of digital platforms.

Turtlemint’s hybrid model, centred on its network of Digital Partners, differentiates it from pure-play online marketplaces. However, it also places the company in direct competition with a broader set of distribution channels operating across both offline and online formats.

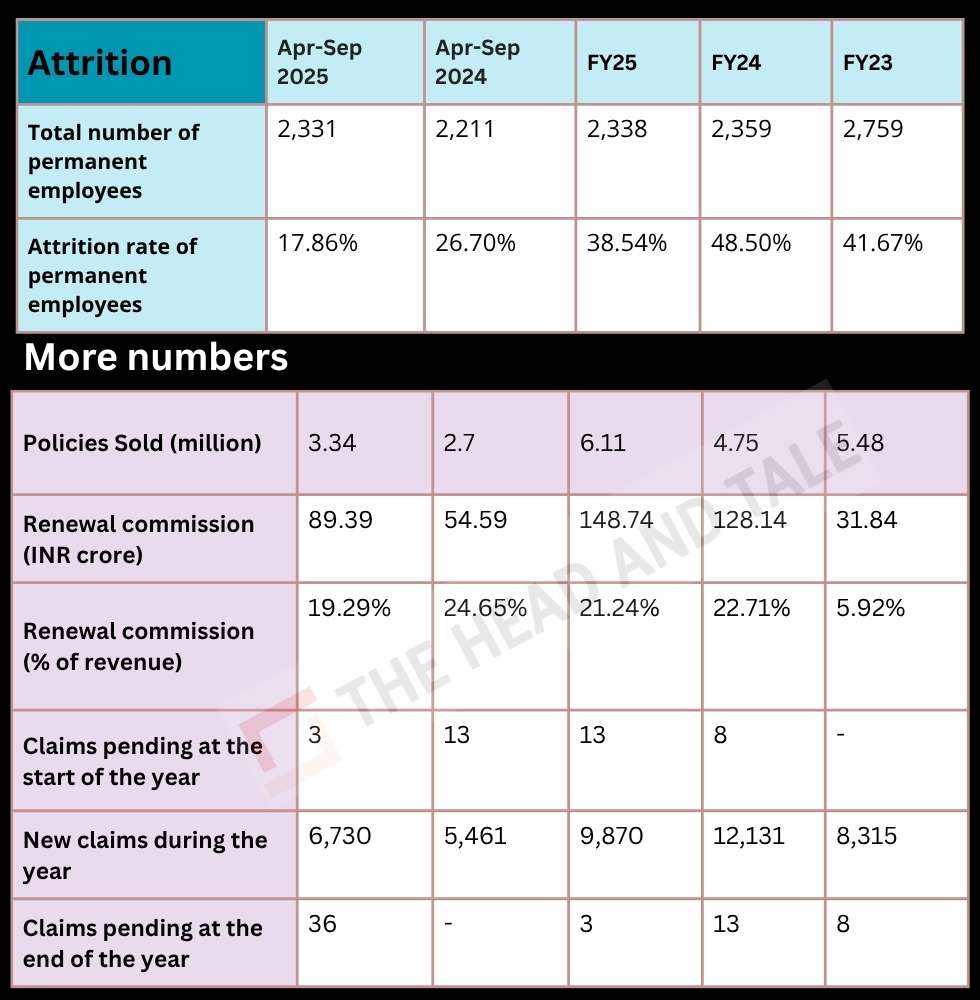

This competitive intensity is also reflected in employee attrition. While the company’s attrition rate declined to 38.54% in FY25 from 48.5% in FY24, it remains elevated. “The attrition rate for our permanent employees… was primarily due to competition for experienced talent in the technology sector, higher turnover within our sales organisation and increased demand for specialised digital skills,” the company noted in its UDRHP.

The industry has also seen consolidation, with InsuranceDekho merging with Apis Partners-backed RenewBuy, underscoring intensifying competition despite a large addressable market. The deal received approval from the Competition Commission of India last year.

At the same time, barriers to entry in digital distribution remain relatively low, particularly with rapid advances in artificial intelligence. As technology adoption deepens, newer players can replicate parts of the model, intensifying competition not just from established platforms but also from emerging startups.

“These AI-first companies may require significantly less capital…allowing them to compete effectively with us,” the company noted, adding that such competition could adversely affect its market share, business prospects and financial performance.

GST dispute

The company is also facing a GST-related exposure, with tax authorities confirming penalties aggregating to around Rs 512 crore for the period between 2017 and 2023.

The demand arises from orders passed by the Directorate General of GST Intelligence, which has alleged that the company raised invoices on insurance partners without actual provision of services between FY18 and FY23. This is materially different from typical GST disputes involving classification or input tax credit, as it directly questions the substance of revenue recognition. The company has contested the findings and filed appeals, and accordingly, the amount continues to be disclosed as a contingent liability.

However, the scale and nature of the allegation, coupled with the fact that the exposure has increased over time, suggests a deeper regulatory scrutiny of its earlier business model, particularly around marketing fee arrangements.

An adverse outcome could result not only in a significant cash outflow but also raise concerns around accounting practices and compliance standards.

Reliance on top insurers, general insurance and few states

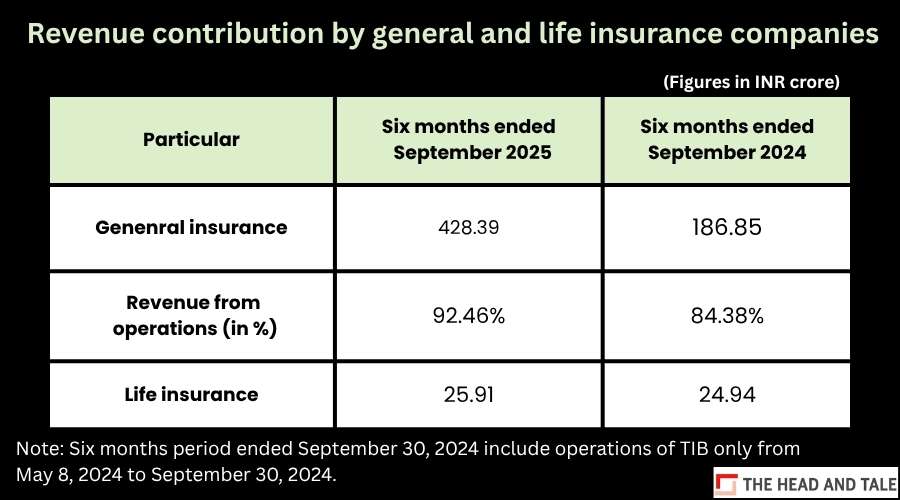

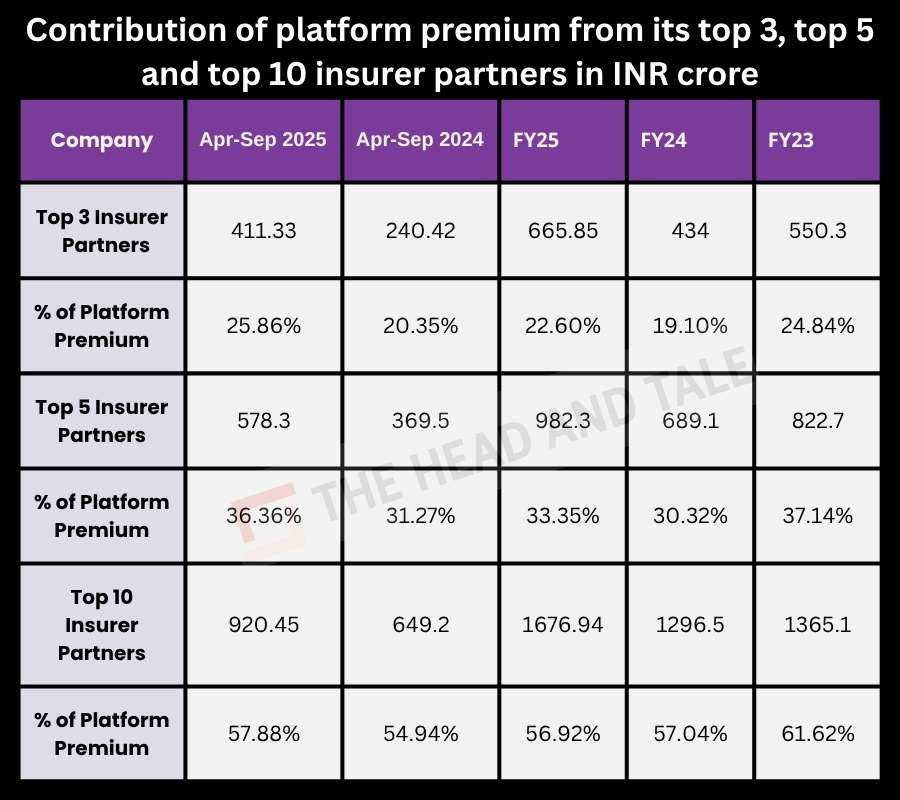

The company also remains heavily reliant on general insurance, particularly motor insurance, which continues to account for the bulk of its revenue. General insurance contributed over 90% of revenue from operations in the six months ended September 30, 2025, underscoring a high degree of concentration. While this segment has driven scale, it also limits diversification, leaving the business exposed to any slowdown in motor insurance demand or changes in product economics.

This concentration is further visible in its dependence on a relatively small set of insurer partners. The top 10 insurers accounted for over 70% of revenue in the latest six-month period, indicating that a significant portion of the business is tied to a handful of relationships. Any adverse changes in commission structures, product availability or partnerships could have a disproportionate impact on revenue.

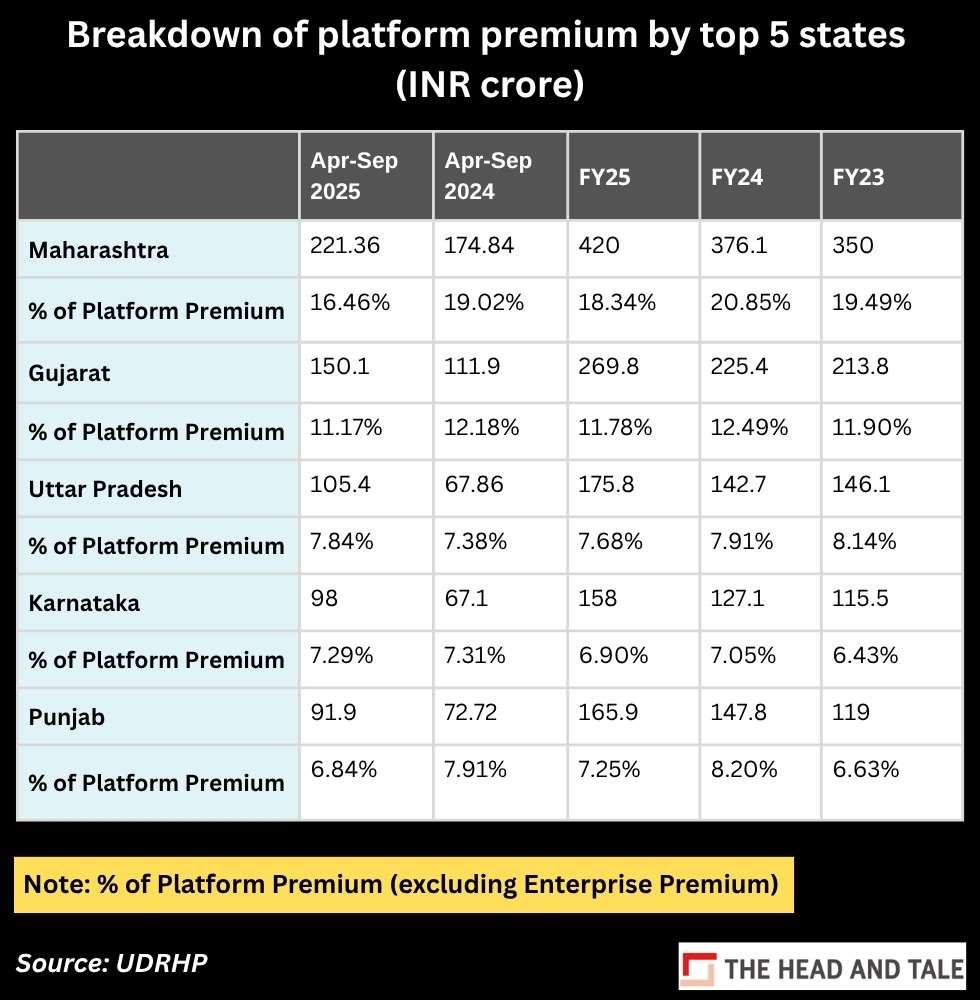

Geographically, the business also shows concentration, with Maharashtra and Gujarat together contributing close to a third of platform premium over the past few years. While these are large and economically significant markets, such dependence exposes the company to regional risks, where any slowdown or disruption in these states could weigh on overall performance.

New businesses

Beyond its core insurance distribution business, Turtlemint has also expanded into adjacent financial services over time. The company entered the mutual funds segment in FY21, followed by the introduction of lending and deposit products in FY24. These additions reflect an attempt to deepen engagement with its existing network of Digital Partners by enabling them to distribute a wider suite of financial products through a single platform.

The company has also extended its advisor-led model to enterprise partnerships through the launch of Turtlefin, a digital insurance distribution platform tailored for corporates. While these initiatives broaden the company’s addressable market, they remain relatively early in their development, with competition already intense across each of these segments.

“We have limited experience in offering financial products, which may affect our ability to successfully market, sell and manage these products,” it said.

The UDRHP also noted that its mutual fund business -- Turtlemint Mutual Funds Distributors Pvt Ltd -- has incurred losses in the past. In the six months ended September 30, 25, however, the mutual fund business had clocked a small profit of Rs 19.2 lakh.

Ultimately, while the opportunity in insurance distribution remains large, but with Turtlemint’s evolving business model and shifting revenue mix, the question for investors is not just about the size of the market, but whether Turtlemint can translate its scale into sustainable and predictable performance over time.

Justice M Nagaprasanna ruled that the arrests were contrary to law while hearing petitions filed by the founders challenging their detention under the Prevention of Money Laundering Act (PMLA). A detailed copy of the judgment is awaited.

The ED had arrested the three founders on May 8 following searches at multiple locations linked to Gameskraft and its executives across Karnataka and the National Capital Region. The agency's investigation stems from multiple FIRs alleging cheating, fraud and other offences linked to the company's real-money gaming operations.

The court order comes weeks after the ED intensified its action against the company. In May, the agency froze deposits worth Rs 526 crore and arrested the founders as part of a money laundering investigation into Gameskraft's gaming platforms, including RummyCulture and RummyTime. According to the ED, the probe uncovered alleged violations linked to the company's online gaming business.

The case has emerged as one of the highest-profile enforcement actions against India's online gaming sector, which has faced increased regulatory and legal scrutiny over real-money gaming models in recent years.

The Head and Tale mapped companies that have landed on the ED's radar amid an expanding crackdown on alleged online gaming fraud, money laundering and regulatory violations.

]]>