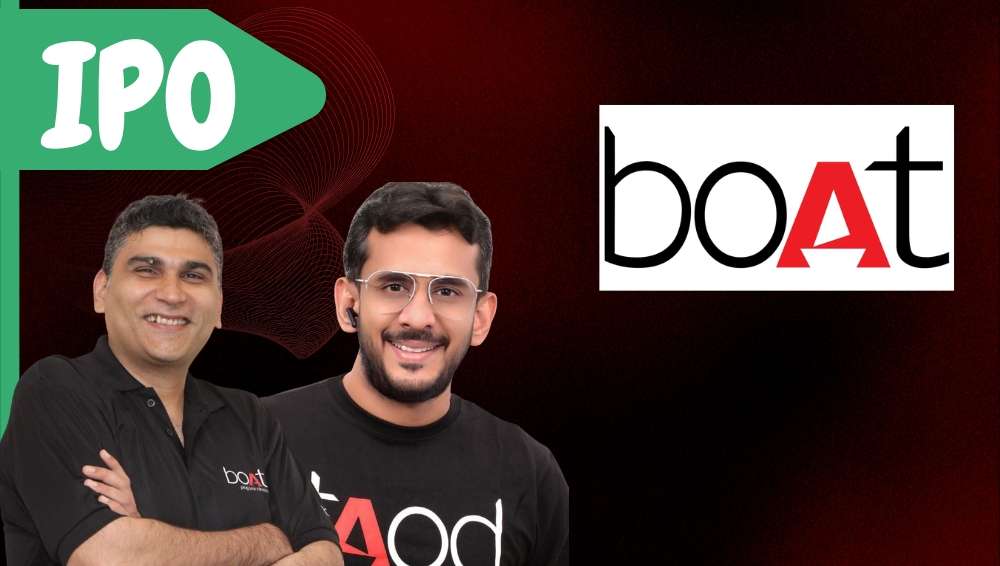

Boat IPO: A second shot amid management shake-up, flat revenues, eager to exit investor

26 Nov 2025, 03:42 PMIn this deep-dive, we look at the time when consumer electronics company Boat had filed the DRHP in 2022 and the point where it may have peaked before it began to slide.

Joseph Rai

Share the story on

Less than a month after Boat received the regulatory nod in September this year for its initial public offering (IPO) filed via th

Subscribe to read the full story

Stay ahead in fintech leadership with insightful news and ecosystem mastery

Access premium journalism by selecting a Subscription Plan

1 Year

$ 99.00

Who Reads Us

“I enjoy reading The Head and Tale for their coverage on the Fintech landscape. The reporting is incisive and honest, and it demonstrates a sharp understanding of the industry and the issues that concern it. I'd like to extend my best wishes to Arti for her continued success.”

“Well-researched, informative and analysis based reporting makes an interesting read. 'The Head and Tale' news portal has been demonstrating this quite well covering fintech and emerging tech sectors. Their timely updates, exclusive stories and different perspectives on these sectors help me stay informed. Kudos to Arti Singh for pursuing her passion and best wishes to the team.”

“The Head and Tale stands out for its deep industry knowledge and impressive network of sources. I especially appreciate that the reporting remains independent, rarely resorting to paid puff pieces, making it a publication I can genuinely trust. Having followed Arti’s work for years, I’ve come to rely on The Head and Tale for its unparalleled insight and truly independent coverage. Arti’s long-standing presence in the sector means her reporting is always informed, with access few can match.”

“What I really appreciate about The Head and Tale is that it doesn’t just report the news, it interprets it. The stories are well-researched, comprehensive, and bold. Arti brings a fearless lens to reporting, often asking the uncomfortable but necessary questions. She makes you pause, reflect, and rethink what it all means for the payments and fintech ecosystem. It’s rare to find journalism that’s this sharp, timely, and relevant to the work we do every day.”

“I’ve always valued journalism that goes beyond surface-level headlines. The Head and Tale does exactly that - it connects the dots, asks the tough questions, and brings clarity to the shifts shaping our evolving industry. I’ve even encouraged my team members to subscribe, because staying informed through credible, deeply reported stories is as important as building products. For me, The Head and Tale has become part of essential reading.”