The shadow economy of online gaming: How money moves beyond the screen

04 Sep 2025, 06:01 PMBehind flashy apps and jackpots lies a complex web of mule accounts, payouts, and payment tricks that move thousands of crores beyond the screen.

Share the story on

“I gave a contract to someone to build my house in my village in Odisha. The contractor gave Rs 6 lakh to one of his staff for material purchase. But the staff used – or rather lost – the entire money in online gaming. The poor guy’s father had to sell his house to pay off the money,” recounts a senior executive at a fintech company.

This isn’t an isolated incident – and neither you are

hearing such stories for the first time. Ever since the government announced a

ban on online real money gaming, you may have read many similar stories.

The ban itself was prompted by such stories that the regulators kept hearing over and over again – tales of families ruined, salaries drained, and entire savings vanishing into the vortex of real-money gaming apps. The ban has been framed as a moral and financial safeguard: protect citizens from addiction, curb money laundering, and cut the link between UPI and betting.

Before imposing its sweeping ban, the government itself put

numbers to the problem: 45 crore Indians were collectively losing crores of money

to these games. This captures only the tip of the iceberg.

All the headlines showed the impact of the ban only on the

bigger and visible online gaming brands like Dream11, MPL and Zupee among

others. Industry federations lobbied aggressively in their defence, claiming

they were creating some 2 lakh jobs and paying hefty taxes, including the new

28% GST.

But insiders know that brands like Dream11, previously the

title sponsor of the popular IPL cricket tournament, is just the face of the

real money gaming industry.

The real action lies elsewhere. A parallel industry of APK downloads, Telegram betting circles, and offshore portals hidden behind front companies function in the underbelly of the society. On paper, the offshore portals look like “clothing retailers” or “e-commerce startups.” In practice, they are funnels for betting on cricket, rummy, and everything in between.

These online real money games funnel billions through

India’s payments system. While the numbers floating claims that Indians spent

some Rs 10,000 crore a month on online gaming, industry insiders believe this

parallel industry was 4x-5x bigger than that.

Not surprisingly, this parallel industry hasn’t gone away

notwithstanding the government’s swift implementation of the ban in record time

and the harsh punishment it has put in place to deter people from engaging in

real money gaming. Anyone found breaking the law will be imposed a monetary

penalty of Rs 1 crore and three years of imprisonment.

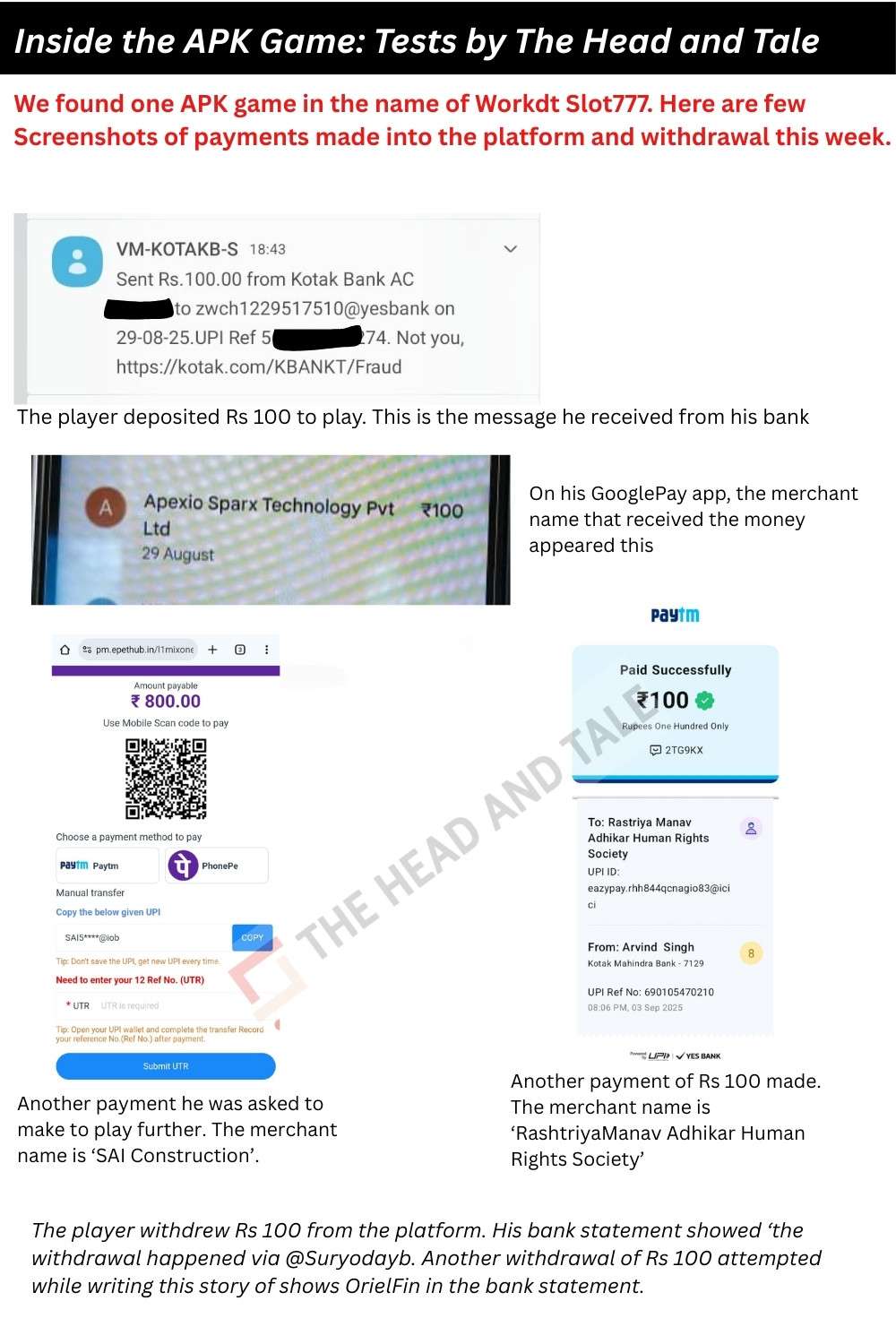

As we write this, APK-based games are still alive – downloadable under innocuous company names, with payments routed through UPI. The Head and Tale conducted few such tests –attempted via Google Pay, PhonePe and Paytm – went through seamlessly (a slight twist though…payments were accepted via QR code). The bank on the other end?

Yes – you guessed it right. It’s Yes Bank.

How the shadow gaming economy works

Let’s explain this with real life anecdotes. Somewhere in a small city in Aligarh a young man launched a gaming app after securing a legal opinion and getting his app cleared for the Play Store. Business boomed – the app was pulling in nearly Rs 8 crore a day.

Marquee gaming brands – Dream11, MPL, Zupee – would turn to celebrity endorsements and TV spots to draw users. But shadow operators like the young man in Aligarh uses a very different playbook. Their reach come through closed networks: pirated movie files on Telegram seeded with APK links, relentless forwards in WhatsApp groups, and small referral chains that incentivises users to bring in friends.

It is a well-crafted strategy. By bypassing app stores and mainstream advertising, these platforms keep themselves off regulators’ radar while ensuring rapid distribution. Once a user installs an APK, the cycle reinforces itself – friends push it to friends, operators sweeten the deal with referral payouts, and Telegram piracy channels act as the biggest billboard no one could regulate.

In short, these aren’t games discovered by accident; they

are planted systematically in the places – invisible to regulators, but visible

to those who know where to look.

Then, comes onboarding.

Once a player finds a game, the real question is how money moves in and out. That’s where the entire machinery of onboarding comes in – “a system designed to fool banks, regulators, and even payment companies themselves (a theatre of compliance that all sides pretend to believe).”

To enable this, there are intermediaries involved. For

instance: in one case, there was a broker based in Mumbai – a middleman linked

gaming merchants like the young man in Aligarh – with payment aggregators/gateways,

and banks. The broker ensures that the gaming merchant has not just one but two

leading aggregators, including a backup. At one point this Mumbai broker had

stitched together deals for three poker and rummy platforms. At their peak,

these three platforms were doing around Rs 1,500 crore in transactions every

month.

Similarly, a Delhi-based professional who worked and interacts with gaming merchants recalled how an intermediary once approached him, claiming to handle several “e-commerce” merchants with daily volumes of nearly Rs 1,000 crore. “I was clear this couldn’t be e-commerce,” the person said. “Later, I found the merchants were running games exclusively through APK files.” The trick was simple: the intermediary used a Third-Party Service Provider (TSP) – a payment gateway that itself cannot do settlements but partners with a bank that can.

The pattern repeats across the ecosystem. APK-based gaming

operators avoid registering as gaming merchants; instead, they mask their

identity behind fronts such as textile shops or trading firms.

A former payments executive of a payment gateway firm

SafexPay explained that gaming merchants approach payment gateways, saying they

are involved in e-commerce or trading, and get onboarded like any other

merchant. SafeXPay worked (works) with four-five big gaming clients had

stitched a deal with a bank in the backend to process and settle these

transactions. The company, whose payment aggregator application was rejected by

the Reserve Bank of India, has been under ED scanner couple of times over past

few years.

There are many like the SafexPays in the market.

The trick lies in appearances, another source noted. Gaming merchants set up front companies – textile shops, trading firms, watch retailers. So, when a bank officer or a payment aggregator sends someone for a site visit for KYC checks, the shop looks genuine with stocks on display, and invoices in place. “On paper, everything is perfect. But suddenly, their transaction volumes would be unrealistic. And, during IPL, it would jump. Who is going to buy clothes worth Rs 100 in such huge numbers?” the source revealed.

Behind the onboarding process sits a chain of intermediaries – brokers who connect merchants to payment aggregators/technology service providers (TSPs), and banks. One Delhi-based source described it as: “There are always four or five layers behind one merchant. A bank relationship manager/senior official, someone handling cyber issues, even accountants who know how to make it look clean, and the broker. Everyone takes their cut.”

A buzz in the market, according to the Delhi-based

professional mentioned earlier, also suggests that some senior bank officials

would involve in a way where they would set-up entities under their family

members’ name and the commission would flow into those entities.

Banks typically charged around 0.5% for UPI transactions in

risky segments, which translates to a substantial income on high volumes.

Mediators marked up that rate, charging gaming merchants 2-2.5% and pocketing

the difference.

For banks, one of the biggest red flags in onboarding a new merchant is the rate of chargebacks – disputes raised by customers asking for their money back. High chargebacks usually signal fraud or risky business. But in the gaming world, insiders say these checks were often managed with a workaround.

“As soon as a chargeback came in, the instruction was

simple: refund it immediately,” recalled one payments executive. “In the system

it must look like the issue is resolved quickly. This practice kept chargeback

rates artificially low. If the percentage stays around 2.5-3%, banks treat it

as manageable,” the executive added. “That was the sweet spot for getting

merchants onboarded.”

Only when chargebacks piled up and reached the RBI’s radar

would the true scale of the problem become visible.

Having said that, the real innovation was how transactions

appeared to players. Depositing money into these APK gaming platforms rarely

showed the same merchant twice. Instead, each payment carried a different name.

A source familiar with the process said: “It’s dynamic UPI, where the name

keeps changing everytime a player deposits money. If you pay four times, you’ll

see four different merchant names.”

One gaming company but multiple entities puzzle

To stay ahead of scrutiny, operators float multiple entities

with different directors, each having new e-commerce sites. Interestingly,

the gaming merchant builds a system and integrates it in a way that each time

someone goes to a payment page, there is this dynamic PG changing in the

backend. “It’s easy to set up 20-50 companies and present them as different

merchants. Each one becomes another pipe,” a payment aggregator employee said.

What really made detection difficult was how transactions

were routed. Normally, when a payment happens, a payment aggregator pings an

acquiring bank with the merchant details. In gaming, those details were

deliberately scrambled. A payments industry official explained: “The

transaction might originate under one merchant ID, but by the time it reaches

the bank, it could be showing as another. They have thousands of such setups

ready, so the system keeps switching automatically.”

This meant that if a player made four deposits on the same

app, each one could show a different name. One might look like an e-commerce

site, another might appear under a government-related code, a third under a

trading business, and so on. Each came with a different MCC (Merchant Category

Code), which also changed the transaction fee rates.

[This also explains why the Reserve Bank eventually

started chasing MCC misuse lately.]

Payment aggregators and banks sat at the centre of this web.

Insiders say they were well aware that many of these “e-commerce” merchants

were in fact gaming operators. “Sometimes it’s the company, sometimes it’s an

employee looking the other way,” one source said.

When regulators tightened norms — for instance payment

processors to play safe impose transaction limits at their end. However, even

the limits imposed doesn’t stop them. For example: If one aggregator capped a

merchant at Rs 10 lakh a day, the same merchant would already be live with

other PAs and banks. Once one limit was hit, traffic automatically shifted to

the next. “There’s enough orchestration in the system. A merchant showing Rs 10

lakh at one gateway could actually be doing Rs 1 crore across ten of them,” a

source said.

As one payments industry veteran pointed out: “If you look

at the numbers, India claims 60-70 million merchants. But half the shops are

shut. How can e-commerce be so bustling? The answer is, a big part of it is

gaming money flowing in disguise.”

The Payout Engine

If pay-ins kept the money flowing into gaming companies,

payouts kept players hooked. Every Rs 100 deposit might fund the occasional

jackpot winner, but far more important were the thousands of small returns – Rs

200 here, Rs 500 there – that gave players the sense they were winning and

encouraged them to play again.

“Gaming was as much about payouts as it was about

collections,” said one payments industry insider. “Out of 10,000 players, 9,000

got something back. That required a massive, industrial-scale payout system.”

This is where payout APIs became indispensable. These tools,

offered by banks and payment players, allowed gaming firms to disburse

thousands of micro-payments instantly into users’ accounts. The business grew

so fast that, at one point, insiders estimate gaming and domestic money

transfer business dominate the payout API usage.

The economics made sense. Banks charged flat rates per transaction – roughly Rs 1.50 for amounts up to Rs 999, Rs 2.50 for payments from Rs 1000 up to Rs 25,000, and Rs 3.50 (sometimes Rs 5) beyond that. And, then the ecosystem intermediaries add approximately Rs 3 on top of it as their own margins. Given that gaming generated millions of small-ticket payouts daily, the business was a goldmine.

But the scale also strained systems. “Cosmos tried it, South

Indian Bank tried it. The systems burst under the pressure of so many

micro-transactions,” recalled another person familiar with the matter.

Many firms outsourced their payout operations to third-party

service provider (TSP). “If I’m a gaming company, I could simply give my bank

account credentials to a payment player (TSP) and let them run payouts

operations – which is a grey area,” said a source. “A lot of this business has

evolved around the money going straight to the gaming company account through

payout APIs.”

Regulators eventually moved to separate pay-ins from

payouts, forcing payment aggregators to not mix the two businesses.

Even then, the payout gold rush had already reshaped the

payments industry. According to multiple insiders, Yes Bank became the biggest

beneficiary, distributing payout APIs widely. “Other banks include IDFC First

Bank, and Suryoday Small Finance Bank. Among payment companies, Razorpay and

Cashfree and a clutch of smaller players were deeply embedded in the gaming

ecosystem,” a source said.

Money laundering problem

While gaming apps were a lucrative business for local gaming

merchants, banks, and payment companies, the government grew increasingly

worried about something else: the way these platforms were being misused for

hawala, cryptocurrency laundering, and Ponzi-style flows.

As noted earlier, on paper, most of these operators didn’t even look like gaming firms. They registered themselves as e-commerce companies – “XYZ Textiles Pvt Ltd” or “ABC Electronics” – and quietly processed thousands of small UPI payments, usually Rs 100-Rs 500 each. To an ordinary user, it looked like just another online purchase.

The problem – money rarely stayed in India. Offshore operators, mostly based in Dubai and Singapore, had struck deals with local (proxies) partners. Once the payments came in, funds were often converted into USDT [a stablecoin pegged to the dollar] via cryptocurrency exchanges – and swept out of the country.

A person aware of this ecosystem and how it operates

explained, “The party sits in Dubai. The business runs here.”

“The laundering mechanics were deceptively simple: Users

make dozens of micro-payments to a front merchant posing as an e-commerce firm.

The bank and PAs settle the money into local accounts – which is routed to

intermediaries who either move it via hawala channels or convert it into USDT.”

In some cases, these flows also served as a way to convert

black money into white. A person described how it worked: “If someone in

Singapore wants to clean his cash, he connects with trusted person in India who

– takes a 1-2% cut – gets thousands of individuals under him. They will be

given Rs 100 and asked to go on gaming app, where they have to go and make a

payment of Rs 100 and earn Rs 10. The players get Rs 100 into an app

wallet, and rewarded Rs 10 for the effort. For players, it was a simple

cashback scheme,” another payments executive explained. “In this flow,

banks/PAs will do the settlement. There is no way banks and PAs would be

able to identify the source of the money they are settling.”

Another instance is when players land on those e-commerce

sites, they would see a regular storefront. But once they clicked through, the

trail often led to an offshore gaming platform.

These international sites maintained deposit accounts where

Indian users were asked to push their money. From there, funds were shuffled

through layers of mule accounts. Another mule account was used to pay out

“winnings” back in India.

This cycle turned gaming platforms into an efficient

parallel banking system, hidden in plain sight.

It should come as no surprise to anyone that all of the

money flows through UPI as cards are blocked by filters and net banking is too

clunky. UPI and QR codes have become the default rail. Insiders estimate that

betting and gaming transactions account for 30% of UPI’s overall volumes.

A payments executive calls it “digital’s paradox”. “UPI was

meant to democratise payments. But it also democratised money laundering.

Instead of one shady Rs 20 lakh transfer, you now have two lakh Rs 100

transfers. Good luck stopping that.”

Impact of the Ban

Payment aggregators (PAs) and banks always knew gaming was a

high-volume, high-margin business. The ban has now exposed how dependent parts

of the financial system had quietly become on these flows.

On the payments side, names like Razorpay, Cashfree, Easebuzz, PhonePe and PayU are among those hit hardest. Each of them insists gaming was a small portfolio – but insiders say the volumes tell a different story. “None of these PAs were processing anything less than Rs 2,000-Rs 3,000 crore of gaming payments every month – and even more in case of some PAs,” one aggregator executive said.

Banks were no less conflicted. With lending margins under

pressure, even a sliver of this market was irresistible. For banks, the math

was simple: a 0.5% fee on Rs 2,000-Rs 3,000 crore of monthly flows meant Rs

10-15 crore every month — enough to move quarterly targets.

“Yes Bank developed a reputation for being loose in structure – open to pilots, proof-of-concepts, and onboarding new players quickly,” one insider said. “Everyone knew it wasn’t textiles. But nobody wanted to lose the revenue. RBL Bank, payments banks like Fino Payments Bank (at one point), and many small finance banks also powered gaming. Their digital-only nature and weak KYC controls made them easy to misuse.”

Interestingly, most of the impact may not even show up under the “gaming” label. Instead, the so-called e-commerce portfolios of banks and PAs – where many gaming merchants were disguised – could take the heaviest hit.

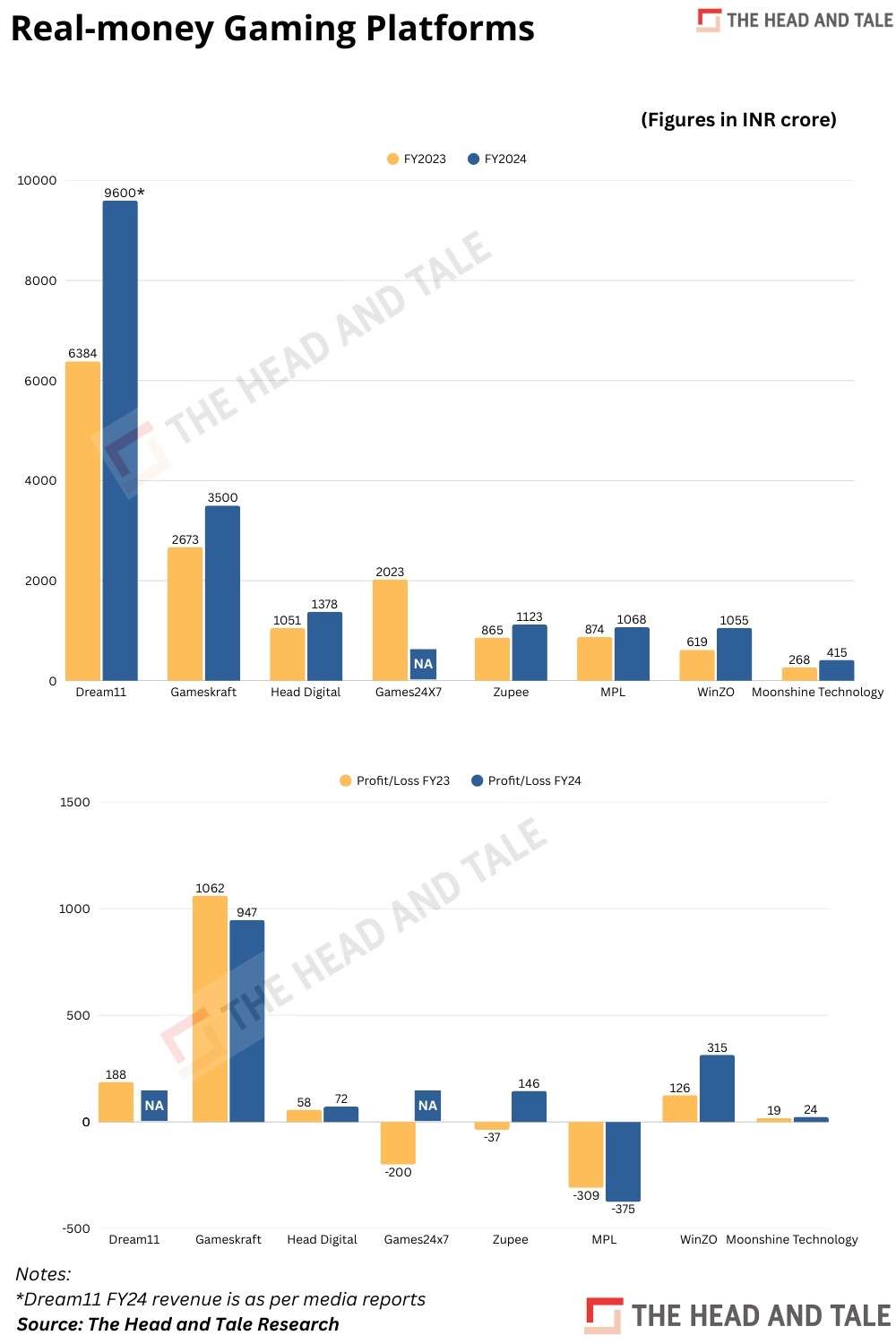

On paper, the revenue impact seems huge. Government

officials say the ban could cost up to Rs 20,000 crore in GST. Industry numbers

peg the annual revenue of the real-money gaming sector at around Rs 30,000

crore.

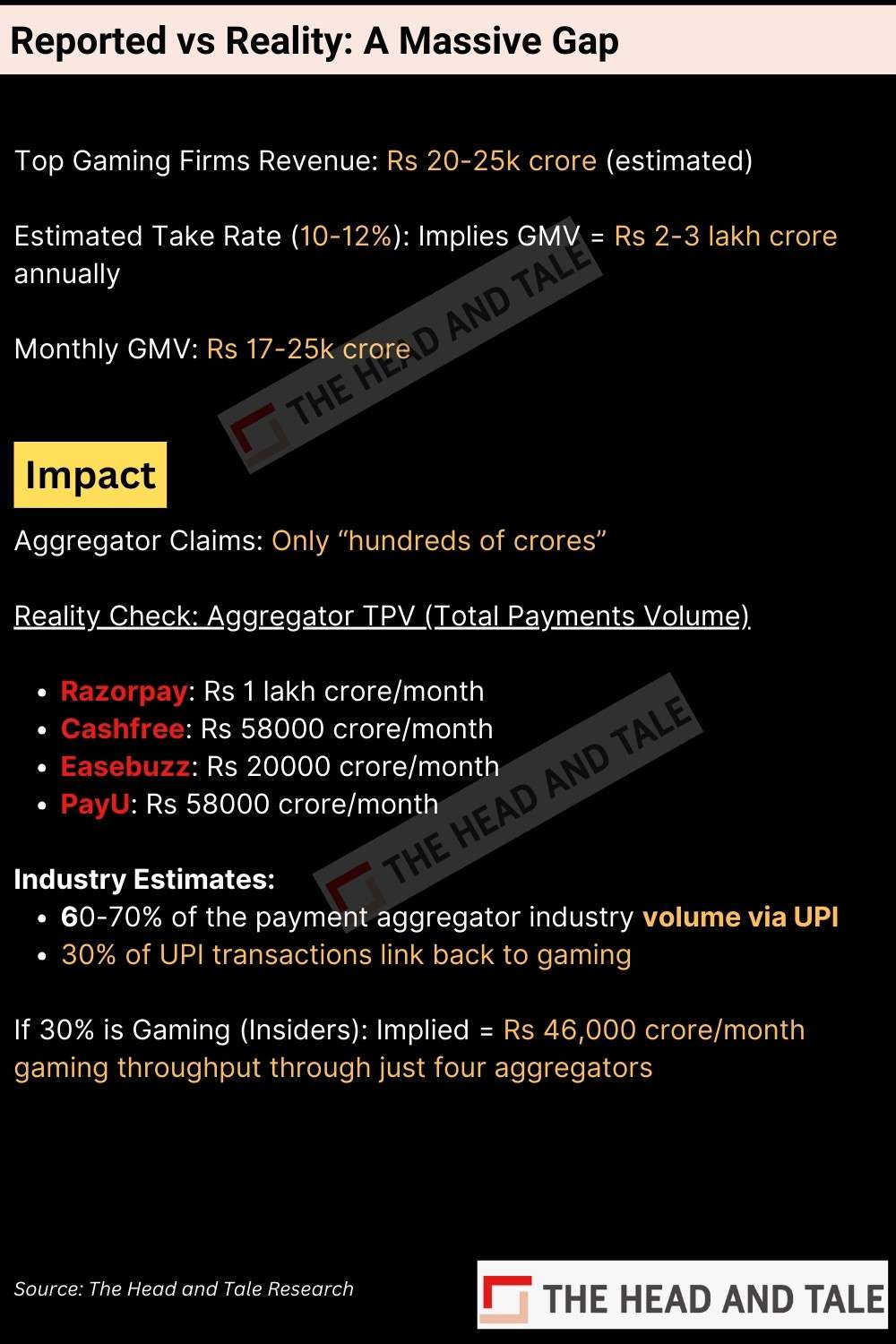

Collectively, the top 8-10 gaming companies show revenues of Rs 20,000-25,000 crore. But here’s the catch: these revenues represent only the “take rate” – the commission the companies earn. If the average take is 10-12%, the underlying throughput (GMV) must be in the range of Rs 2-3 lakh crore. And, the monthly GMV should ideally be in the range of approximately Rs 17000-Rs 25000 crore.

Yet payment aggregators in media reports claim their gaming

volumes are only in the hundreds of crores.

The math doesn’t add up. Here's a back of the envelope calculation:

Razorpay’s annual payment TPV is

$180 billion, which is roughly $15 billion (about Rs 1 lakh crore) monthly

throughput. Cashfree Payments clocked total payment volume of $80 billion

(which is about $7 billion or Rs 58000 crore monthly); Easebuzz's payment

transaction volume hit $30 billion (close to $2.5 billion or Rs 20000 crore a

month); and PayU’s TPV was $80 billion in FY25 (about $7 billion or Rs 58000

crore monthly). Together, just these four companies process $31.5 billion, or

Rs 2.4 lakh crore a month.

Besides, with 60-70% of the payment aggregator industry

volume coming from UPI – and insiders suggesting 30% of UPI transactions

linking back to gaming, the implied gaming throughput is closer to Rs 46,000

crore (approximately $5.6 billion) a month.

That’s far above the Rs 600-700 crore monthly numbers these

companies admit to. PhonePe’s payment aggregator volume is not known. However,

PhonePe’s UPI transaction volume is going to be impacted the most.

Other than these, 55 players have received final payment

aggregator licence so far from the RBI. For many small companies, gaming became

majority source or only source of revenue.

The discrepancy suggests two things: one, a big chunk of gaming payments may be routed under other merchant categories; and two, the true scale of “under-the-radar” platforms – far beyond Dream11 and MPL – could be four to five times bigger than the official industry number of Rs 10000 crore as claimed in media reports.

"Gaming has been one of the most exciting digital sectors in India, and we have always supported innovation. However, it represents only a very small fraction of Razorpay's overall business, especially when compared to the significant growth in sectors like e-commerce, travel, education, and financial services, among others. Having observed the developments over the last few days, we can confirm that the impact on our business is negligible. As the online gaming industry pivots and adapts, we'll continue to explore how we can work with them in future," Razorpay spokesperson said.

"Our engagement with gaming merchants has always been limited. We partner only with a very small number of skill-based gaming players, almost all of whom are large, reputable organizations that meet our stringent onboarding and compliance standards. As such, gaming represents only a minor portion of our overall portfolio. Given this measured and controlled exposure, the impact on our overall business is non-existent," PayU spokesperson said.

"Our merchant portfolio is highly diversified, with our largest volumes coming from sectors such as ecommerce, BFSI, travel, and tourism. Real-money gaming companies account for a very small proportion of our overall business. Therefore, we do not expect the government’s ban to have any material impact on our revenues or payment volumes, and we remain on track to achieve our growth targets for the FY," Cashfree spokesperson said.

"Easebuzz has very limited exposure to gaming businesses, with less than 2% of our overall annual GTV. Hence, we don't see any noticeable impact on our revenues. The majority of our business is driven by the core sectors of the economy, with around 50% of revenues contributed by BFSI, 25% from retail, 20% from education, and the rest from sectors like real estate, travel and tourism, etc," said Easebuzz spokesperson.

Is the game over?

Can this industry really be stopped? Not yet – and apparently never, insiders say.

Two things are clear. First, what is visible through the large brands is only the tip of the iceberg. The underbelly – smaller, under-the-radar operators – is much larger and harder to regulate. If it were only five or six big companies, the government could find ways to control them. But the real market lies elsewhere.

Second, while the online share will come down, it won’t

vanish. Some estimate 50-60% of the market will shrink over the next three to

four months. But 100%? Never. Instead, flows are already moving offline.

“Now things are shifting offline, through BC (Business Correspondent) networks,” one insider explained. “Think of a grocery shop owner – he gathers four people, each puts in Rs 100 and starts playing. If one wins, he gets paid, if another wins, he gets paid too. Whatever is left – say Rs 100 or Rs 150 – the shopkeeper keeps his cut and then deposit to the operator’s account.”

Cash-based Ludo or poker games are already happening in industrial pockets. In effect, the money flow simply shifts – offline, or into a mix of offline and online.

Moving offline may reduce the addiction a little, but it

won’t stop the flow. “The money these gaming operators were making is massive,

and they’ll look for new hacks or loopholes to keep it going. Many are already

experimenting with offline models, or turning to luck-based games like Tambola,

backed by “legal opinions,” to quietly operate under the radar,” the Delhi-based

industry official added.

“The problem with onboarding at such massive scale is that it relies only on automated checks. So someone can come up, register under any random name, put up a site saying ‘launching soon’ or even ‘teaching party tricks’. Once that’s approved, they can quietly switch to a new app – say, for poker – and start collecting payments. Catching this in real time would mean constant monitoring by payment aggregators, which is practically impossible,” a top payment aggregator official said.

That’s why many argue the only effective choke point is the banking channel. Unless those pipes are cut, the industry can’t be stopped. When crypto was banned, the sector collapsed only because banks shut down access to payment rails. A similar move could throttle gaming. Otherwise, operators will keep finding ways – from QR codes in offline shops to cross-border UPI pipes, even stablecoins and crypto.

This brings us to UPI. For years, its meteoric rise has been held up as India’s biggest digital success story. But if as much as 30% of that volume really came from gaming an betting, the story looks very different. The real test will be during the IPL and the Cricket World Cup. If UPI volumes dip then, it will confirm what insiders long suspected – that gaming was one of UPI’s hidden engines.

Will the government allow that to show? Unlikely. NPCI might

“flatten” the numbers, showing only a small dip while framing it as proof that

they’ve curbed online gaming. Optically, everyone would want at least one month

of lower volumes to showcase the impact of the ban.

The fallout for payments firms could be sharp. PhonePe and Razorpay, both preparing for IPOs, face a double blow – lost volumes and lost margins. PhonePe may find it easier to make up numbers through consumer cashbacks and recharges. But B2B players like Razorpay, Cashfree, and Easebuzz are hit harder. Unlike zero-MDR UPI, gaming flows gave them a fee cushion that helped margins. Losing that revenue stream is not easy to replace.

So, is the game really over for the industry? Unlikely. The rules have changed, the channels may shift, but the money will keep flowing – one way or another.

The author is Founder and Editor of The Head and Tale. She can be reached at

[email protected]

Tweets @artijourno

Who Reads Us

“I enjoy reading The Head and Tale for their coverage on the Fintech landscape. The reporting is incisive and honest, and it demonstrates a sharp understanding of the industry and the issues that concern it. I'd like to extend my best wishes to Arti for her continued success.”

“Well-researched, informative and analysis based reporting makes an interesting read. 'The Head and Tale' news portal has been demonstrating this quite well covering fintech and emerging tech sectors. Their timely updates, exclusive stories and different perspectives on these sectors help me stay informed. Kudos to Arti Singh for pursuing her passion and best wishes to the team.”

“The Head and Tale stands out for its deep industry knowledge and impressive network of sources. I especially appreciate that the reporting remains independent, rarely resorting to paid puff pieces, making it a publication I can genuinely trust. Having followed Arti’s work for years, I’ve come to rely on The Head and Tale for its unparalleled insight and truly independent coverage. Arti’s long-standing presence in the sector means her reporting is always informed, with access few can match.”

“What I really appreciate about The Head and Tale is that it doesn’t just report the news, it interprets it. The stories are well-researched, comprehensive, and bold. Arti brings a fearless lens to reporting, often asking the uncomfortable but necessary questions. She makes you pause, reflect, and rethink what it all means for the payments and fintech ecosystem. It’s rare to find journalism that’s this sharp, timely, and relevant to the work we do every day.”

“I’ve always valued journalism that goes beyond surface-level headlines. The Head and Tale does exactly that - it connects the dots, asks the tough questions, and brings clarity to the shifts shaping our evolving industry. I’ve even encouraged my team members to subscribe, because staying informed through credible, deeply reported stories is as important as building products. For me, The Head and Tale has become part of essential reading.”