Fractal IPO: A bountiful harvest for PE investors, now comes the real AI test

15 Dec 2025, 04:41 PMWith its steady track record of giving timely exits to its investors, Fractal marches towards the IPO. But the larger question now is whether Fractal can keep pace with an AI ecosystem...

Joseph Rai

Share the story on

When Fractal Analytics raised its first institutional funding from private equity firm TA Associates in 2013, more than a decade after its launch, the idea of branding itself as an artificial intelligence (AI) company was still a distant notion.

At the time of the funding, Fractal, which was founded by Srikanth Velamakanni, Pranay Agrawal, Nirmal Palaparthi, Pradeep Suryanarayan and Ramakrishna Reddy, was primarily seen as an analytics major that had evolved from a small data firm way back in 2000.

In the 13 years period, the company had raised angel funding from venture capitalist Sasha Mirchandani.

Interestingly, it had also gone through its share of turmoil with three of the founders having already exited the company.

Still, Fractal Analytics pressed on despite the big management churn.

First signs of AI

The first sign of Fractal moulding into an AI company came in mid-2016 when Khazanah Nasional Berhad, the strategic investment fund of the Government of Malaysia, announced a whopping $100 million investment. In a press statement, Co-founder Velamakanni stated, “The investment from Khazanah will help us invest further in our AI & deep learning based software stack.”

The Khazanah investment underlined Fractal's steady growth and it was not long before it attracted another major private equity player Apax Partners as a new investor, which poured $200 million for a significant minority stake. The deal comprised of primary and secondary components, which meant acquiring stake from existing shareholders and paving the way for their exit.

But more than providing liquidity for the existing investors, the most striking aspect during Apax Partners’ investment in Fractal was the categorical recognition of Fractal as “a global provider of AI” to Fortune 500 companies.

Notably, following the investment from Apax Partners, Fractal's business got another thumping validation as it attracted a massive $360 million from new investor TPG in January 2022. The transaction again comprised of primary and secondary components, giving partial exit to Apax Partners.

Still, at that time AI was a term loosely used and did not hold as much weight until the advent of ChatGPT in November 2022 when the concept of AI suddenly became real to the world.

So, when Fractal filed its draft red herring prospectus (DRHP) for its initial public offering (IPO) in August this year, both Indian and global media were quick to label it as India’s first AI company preparing to enter the public markets.

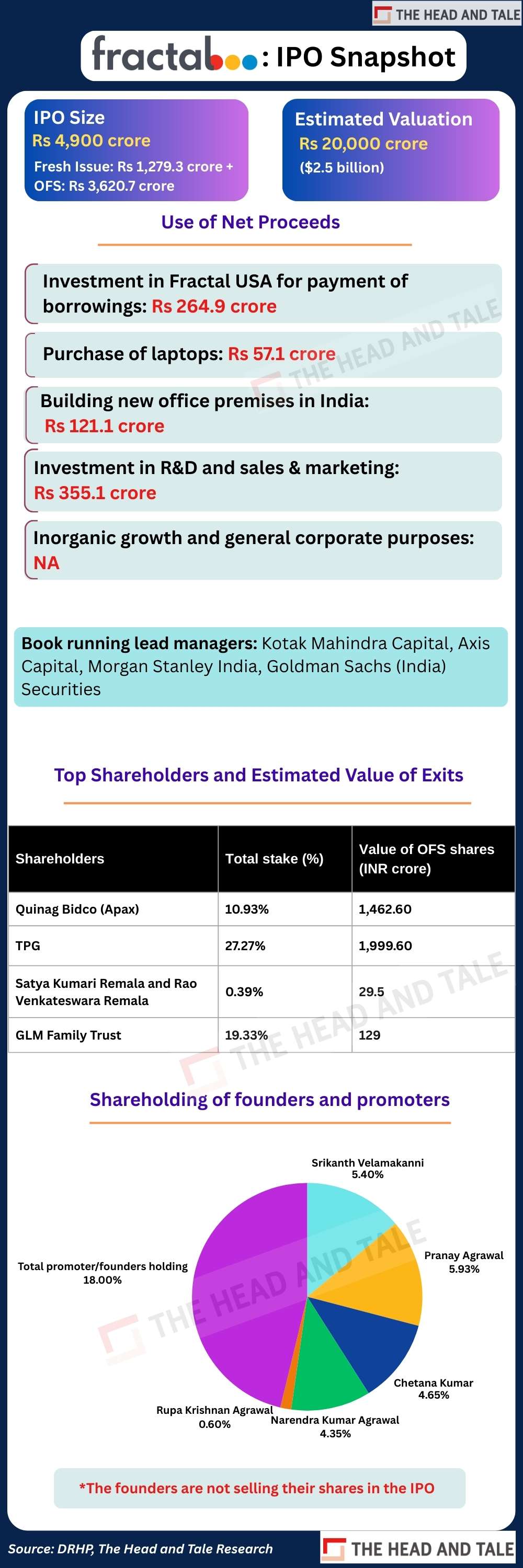

With its steady track record of giving timely exits to its investors, Fractal marches towards the IPO with another liquidity event for its investors on the cards and fresh issue of shares to raise primary capital to double down on its business.

But the larger question now is whether Fractal can keep pace with an AI ecosystem producing new competitors faster than the decades it took Fractal to get here.

As the company itself acknowledges in its DRHP, “The development of artificial general intelligence (“AGI”) has the potential to surpass our current AI capabilities, posing a threat to our business model and potentially rendering our existing AI solutions and AI products obsolete."

We will dissect this risk and more including its significant reliance on its top 10 clients and its dependence on the US as a key geography for its revenue. We will also look into the struggles of its subsidiaries, substantial employee costs, its research and development (R&D) budget and its valuation concerns.

But first let’s look at the monetary value Fractal is unlocking for its investors.

Bountiful harvest

Fractal has been one of those rare companies that would be the envy of other founders and private equity firms that would want not just timely but profitable exits as well.

In a LinkedIn post earlier this year, Velamakanni wrote, “I’ve seen too many entrepreneurs treat investors well on the way in but horribly on the way out. We made sure every investor exited happy.”

Its first institutional investor TA Associates partially exited in 2016 with a reported three-fold gain. While exit figures are not public, the fact that new investors have brought in bigger cheques clearly indicates that the existing investors have walked away with significant gains.

Notably, Fractal also had a pre-IPO fundraise in July this year that involved a secondary sale of 6% stake by Apax Partners to a consortium of 22 institutional investors including private equity firm Gaja Capital. The share sale was reportedly pegged at $172 million. Given that Apax Partners had also offloaded a portion of its stake when TPG invested in 2022, it is clear that the private equity firm has already taken out more than its principal amount.

In the current IPO, Apax Partners is further set to sell shares worth up to Rs 1,462.6 crore via the offer for sale (OFS); and TPG is set to offload stake worth around Rs 2,000 crore.

While TPG invested $360 million in Fractal, its paper gains based on the estimated valuation of the company is $604 million and given its relatively short holding period, it will be clocking a healthy internal rate of return (IRR). Private equity and venture capital firms typically chase an IRR of 20-30% in rupee terms in India.

Fractal has been disciplined in returning capital to investors, but its next phase of growth is likely to be challenging as the AI market becomes more dynamic and hyper competitive.

Risks from AI itself

Fractal is an enterprise data, analytics and AI company (DAAI) and not an AI company in the vein of OpenAI or Anthropic. It supports large global enterprises with data-driven insights and assist them in their decision making through its end-to-end AI solutions. Its AI solutions are organized under two segments: Fractal.ai (comprising AI services and AI products primarily hosted on Cogentiq) and Fractal Alpha (comprising AI businesses), as per the DRHP.

Fractal’s DRHP argues that companies like it are becoming more important because most enterprises simply cannot build or manage AI at the scale, governance standards, or regulatory discipline required today. With talent shortages intensifying and data-governance rules tightening, many organisations lack the in-house capability to deploy advanced AI systems responsibly.

DAAI specialists like Fractal fill that gap. They assemble large, skilled AI teams, bring mature governance frameworks, and help enterprises adopt AI without compromising trust, compliance, or cost controls. In other words: as AI becomes more complex and regulated, the need for specialised third-party providers only increases.

While the DRHP expounds on the opportunity in the space that a DAAI company like Fractal can tap into, it also underlines how the developments around AI pose significant risks.

According to the DRHP, the pace of innovation in AI, especially in generative AI, is now so fast that tools, models and frameworks have a much shorter shelf life. Enterprises struggle to keep up with these shifts, and Fractal warns that this volatility could affect the relevance of its own solutions over time.

The DRHP also flags the risk that generative-AI tools and AI-powered coding agents could enable clients to build AI capabilities internally. If that happens, clients may reduce their reliance on Fractal’s services. The company notes that GenAI-driven automation and low-code workflows can improve IT-services productivity to the point of causing potential revenue erosion for third-party providers like Fractal.

Notably, Fractal’s DRHP flags a significant dependency on open-source technologies for developing and enhancing its AI products. The DRHP also notes a competitive risk in the dependency on open-source as rivals can freely use the same open-source base to build competing AI tools, often faster and at lower cost. Some may even offer such software for free, creating pricing pressure and potentially reducing demand for Fractal’s solutions.

Offsetting risks from AI

What is reassuring is that Fractal has been congisant of the enormous developments in AI and has done well to build its in-house AI capabilities.

Interestingly, it had established its “Fractal Sciences” program way back in 2012 to strengthen its R&D creation and to cater to AI demand. The company has built its own foundation models: Vaidya.ai (medical multi-modal foundation model ecosystem consisting of LLMs, VLMs and medical reasoning systems) and Fathom-R1-14B (open source large reasoning foundation model). The company is investing further to enhance reasoning in its foundation models. It has launched Project Ramanujan to develop advanced reasoning capabilities, including a large model focused on mathematical reasoning. The company is also building Pioneer, a multi-agent digital system to streamline the software development life cycle and enable autonomous data science problem-solving.

Fractal has also developed its own Gen AI stack in fiscal FY23 and introduced new Gen AI solutions. The company has launched several consumer-facing GenAI products for public use. These include MarshallGoldsmith.ai, Kalaido.ai, a GenAI-powered text-to-image tool that supports multiple Indian languages, and Vaidya.ai, a publicly accessible GenAI-based medical assistant platform designed to demonstrate AI’s use in real-world settings.

Notably, in September, Fractal was selected as on one the companies by the Indian government to build indigenous AI models under its AI Mission. This will give Fractal access to compute infrastructure, funding and grants, data and model support, faster pilots with government organisations and regulatory and policy backing among others.

But despite the best efforts of Fractal or any other AI company to fortify themselves from the risks AI poses, there is no foolproof shield from the challenges. On the other hand there is also the risks emerging from the chatter around the AI bubble that could affect valuations of AI companies in general.

Based on global benchmarks, Fractal appears to be reasonably valued rather than stretched. According to an Aventis Advisors analysis of AI valuation multiples, the median EV-to-revenue multiple for private AI companies stands at about 23.6x, with enterprise and applied AI firms such as Databricks largely clustering in the 15x-30x range. At an estimated valuation of around Rs 20,000 crore, Fractal’s implied multiple sits close to this global median, making its pricing defensible although sustaining it will depend on the company’s ability to scale platform-led revenues in an increasingly competitive AI market.

R&D investment amount enough?

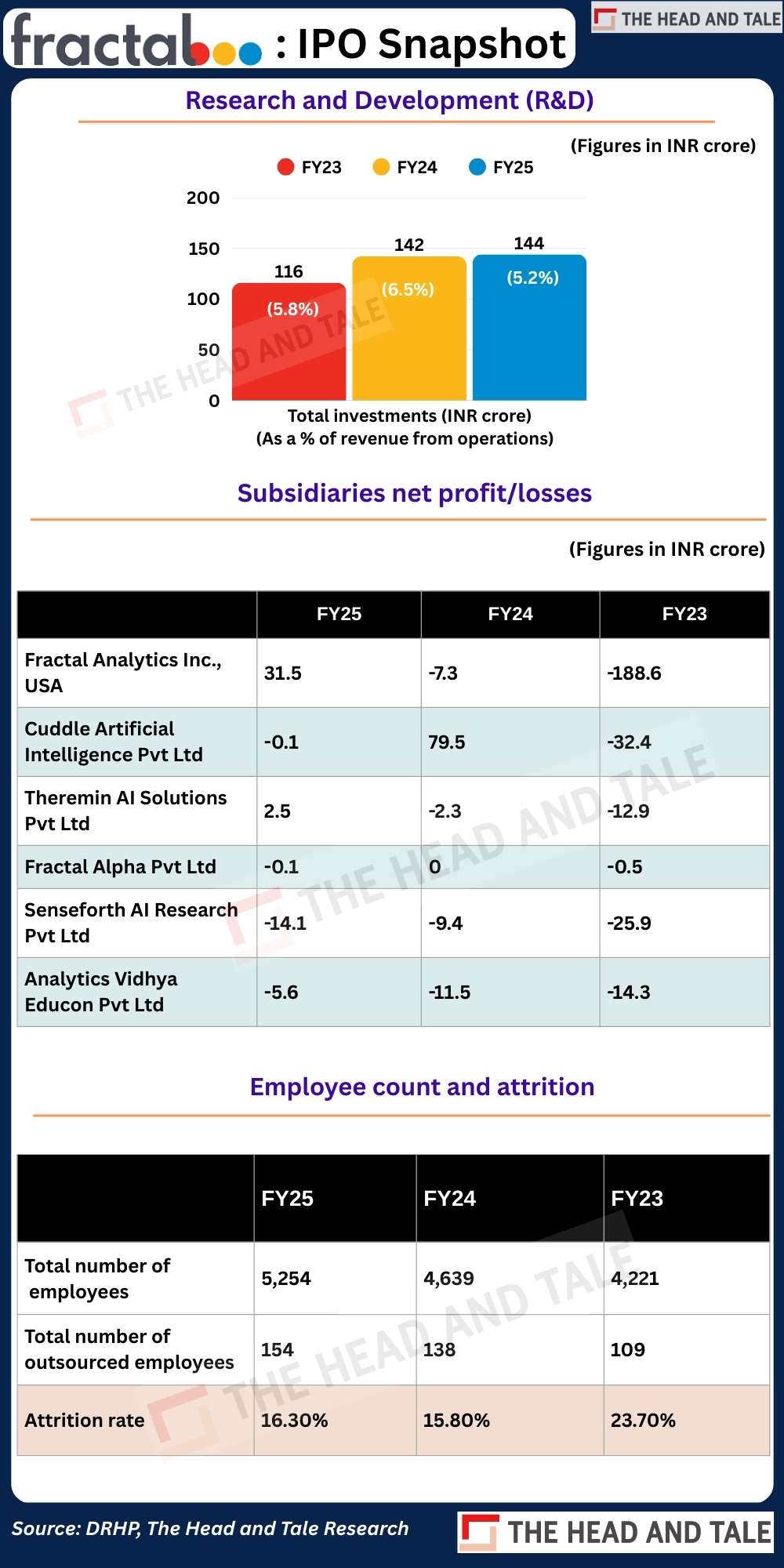

While Fractal has been developing its own AI solutions, its R&D investment has still been measured.

Its R&D allocation increased only slightly to Rs 143.6 crore in the fiscal ended March 31, 2025 from Rs 142 crore in the previous financial year. Besides, its R&D investment as a percentage of revenue shrank in FY25 and it has remained well below the double-digit mark.

Notably, the company intends to use a portion of the capital worth Rs 355.1 crore raised from the IPO for its R&D purposes.

According to an AI-driven intellectual property (IP) analytics platform Relecura, an ideal R&D annual investment range would be 15%-30% of revenue as AI technology evolves quickly, and new models, algorithms, and applications emerge frequently, making continuous innovation essential.

Risks from high dependence on top clients and the US

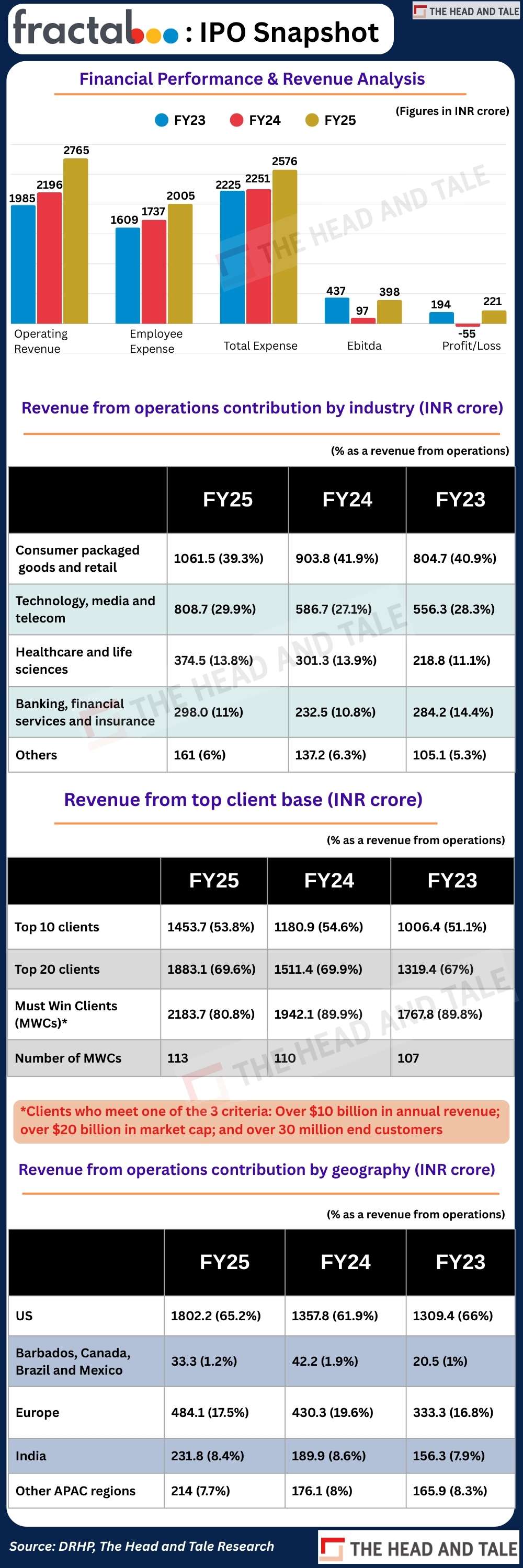

Fractal’s risks also stems from heavy reliance on a clutch of top clients and its significant dependence on US as a market given the volatile geopolitical situation the world has been witnessing.

The company’s revenue from operations from its Must Win Clients (MWCs) has stayed consistently over 80% in the past three fiscal years. MWCs for the companies are ones which meet one of the three criteria: one over $10 billion in annual revenue; over $20 billion in market cap; and over 30 million end customers.

Besides, it has relied upon the US for over 60% of its revenue for the last three fiscal years as well even as India’s contribution is in single-digits, as per the DRHP.

“If we face immigration or work permit restrictions in any country where we have operations, then our business, financial condition, results of operations and prospects may be adversely affected,” said the DRHP.

On the brighter side, its dependence on the sectors appears to be relatively evenly distributed although the reliance on consumer sector is on the higher side. (See infographic)

The company has also highlighted how clients evaluate their partnerships based on their own business performances and may choose to cut their spending.

“For example, one of our top 10 clients in the BFSI industry re-evaluated their essential and non-essential spend as part of an internal restructuring. As a result, while they remain one of our key clients, they have reduced their spend with us,” noted the DRHP.

Overall, the company’s revenue from operations grew 25% year-on-year to Rs 2,765.4 crore in FY25 while it swung to net profit of Rs 220.6 crore from a loss of Rs 54.7 crore. Fractal reported a loss in FY24 mainly because its core business made thinner margins and because it had losses linked to one of its associate companies. While it has reported strong profit in this fiscal, the challenge will be to maintain the momentum.

Risks from subsidiaries and high employee cost

Fractal’s subsidiaries and associate (health tech company Qure.ai that has raised venture capital funding separately) are engaged in the same line of business, and accordingly, have common pursuits with the company.

However, the losses reported by its subsidiaries have been concerning. While Fractal Analytics Inc US and Theremin AI Solutions swung to a net profit in FY5, Cuddle Artificial Intelligence and Fractal AI slipped into a net loss and Senseforth AI Research’s net loss expanded. Analytics Vidhya Educon continued to stay in the red even as its net loss narrowed this fiscal.

The DRHP noted that Fractal USA is its material subsidiary, and as a result, it depends on the results of operations and financial condition of it. “In the event that it incurs losses in the future, our consolidated cash flows, results of operations and financial condition may be negatively affected,” it added.

The company also explained that the losses of the subsidiaries were primarily due to investments in research and development and product support.

“In the event these subsidiaries (apart from Fractal USA) continue to incur losses, we may need to provide financial support which may adversely affect our consolidated cash flows, consolidated results of operations and financial condition,” it stated.

Fractal’s employee cost is three fourth of its revenue from operations. In FY25 it decreased slightly to 72.5% of its revenue from operations from 79.1%. As a data, analytics and AI services company, its high employee cost signals deep talent investment which is critical in a market with acute AI skill shortages. In this sense, high employee costs are almost structural, not accidental. However, in a downturn, Fractal’s people-heavy cost structure could become a constraint if client spending slows and pricing comes under pressure.

Interestingly, the company is also spending Rs 57 crore from its total net proceeds to be raised from the IPO to buy laptops, indicating not just replacements but potential hiring. The company had a total employee base of over 5,250 as of March 31, 2025.

Fractal’s journey from a data analytics firm in 2000 to an AI-led enterprise heading for the public markets has been defined as much by patience as by timing. The company has clearly been successful in giving handsome returns to its private equity investors. We will have to wait and see if the company replicates the same pattern of returning money to its incoming investors as it heads to the public market amid the big and highly competitive AI wave.

Who Reads Us

“I enjoy reading The Head and Tale for their coverage on the Fintech landscape. The reporting is incisive and honest, and it demonstrates a sharp understanding of the industry and the issues that concern it. I'd like to extend my best wishes to Arti for her continued success.”

“Well-researched, informative and analysis based reporting makes an interesting read. 'The Head and Tale' news portal has been demonstrating this quite well covering fintech and emerging tech sectors. Their timely updates, exclusive stories and different perspectives on these sectors help me stay informed. Kudos to Arti Singh for pursuing her passion and best wishes to the team.”

“The Head and Tale stands out for its deep industry knowledge and impressive network of sources. I especially appreciate that the reporting remains independent, rarely resorting to paid puff pieces, making it a publication I can genuinely trust. Having followed Arti’s work for years, I’ve come to rely on The Head and Tale for its unparalleled insight and truly independent coverage. Arti’s long-standing presence in the sector means her reporting is always informed, with access few can match.”

“What I really appreciate about The Head and Tale is that it doesn’t just report the news, it interprets it. The stories are well-researched, comprehensive, and bold. Arti brings a fearless lens to reporting, often asking the uncomfortable but necessary questions. She makes you pause, reflect, and rethink what it all means for the payments and fintech ecosystem. It’s rare to find journalism that’s this sharp, timely, and relevant to the work we do every day.”

“I’ve always valued journalism that goes beyond surface-level headlines. The Head and Tale does exactly that - it connects the dots, asks the tough questions, and brings clarity to the shifts shaping our evolving industry. I’ve even encouraged my team members to subscribe, because staying informed through credible, deeply reported stories is as important as building products. For me, The Head and Tale has become part of essential reading.”